Term Life Insurance

Term Life Insurance Permanent Life Insurance

Permanent Life Insurance No Medical Life Insurance Canada

No Medical Life Insurance Canada Critical Illness Insurance

Critical Illness InsuranceFAQ

Who needs life insurance? We want to protect the people we love. We look after our partners, we build safe homes to raise our children. But what happens when we can’t be there anymore? In the event of your death, life insurance will continue to protect the people who depend on you. Life insurance gives you peace of mind, whether you’re settling down at 25 or 55. By taking out a policy, you shield your loved ones from your personal debt and continue to support them after you pass away. Take control of your debts and protect your family. Take out a policy today. In a world full of uncertainty, life insurance is guaranteed protection.

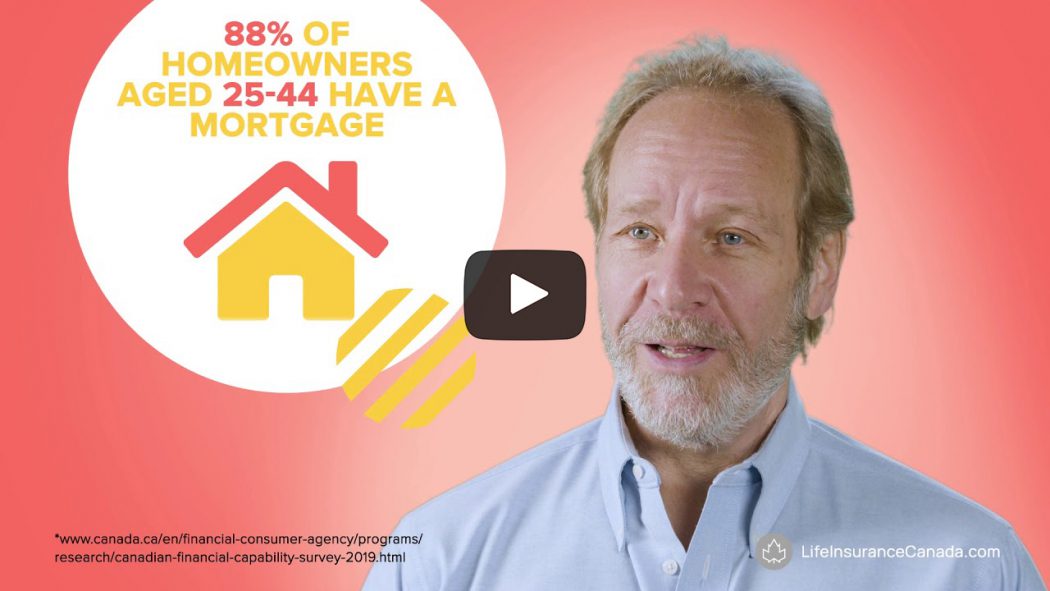

What is mortgage life insurance? Most Canadian households own their homes, but many still owe money towards these homes. 88% of homeowners aged 25 to 44 have a mortgage. If your family is financially dependent on you, your home is as well. Mortgage life insurance takes on the burden of unpaid mortgages. The insurance is tailored to you. In the event of your death, your life insurance policy will cover any remaining debt, protecting both your home and those you love. Let mortgage life insurance help look after your family, even when you can’t be there.

How does term-life insurance work? Ready to take out insurance, but don’t want to commit to a policy for life? Then term life insurance is for you. Term insurance guarantees protection for your dependants within the timeframe of the policy. These policies can cover you from 10 years to upwards of 25. You choose the length of your plan and the amount of coverage you would like. In the event of your death, your insurer will pay out a lump sum, tax-free, to support your family. Term life insurance is cheaper and more flexible than other plans. So, no matter your financial situation, term-life insurance helps you look after the ones you love.

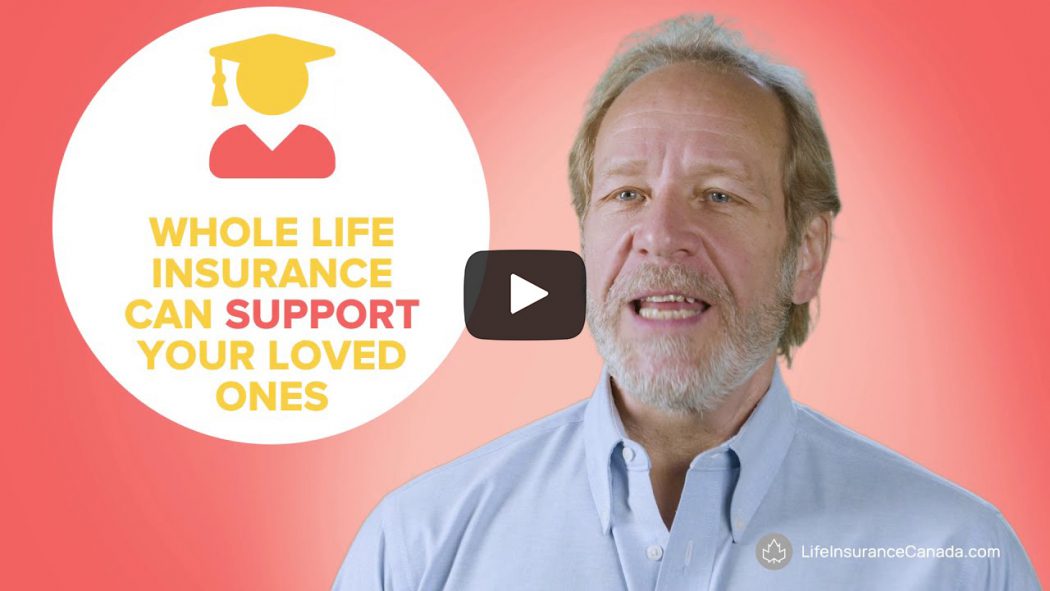

If you’re looking to avoid expiration dates and stressful renewals, whole life insurance is for you! With whole life coverage, you guarantee financial support for your loved ones upon your death, whenever that may be. Your policy will pay out a lump sum to go towards final expenses, estate, unexpected bills, and other living expenses. That’s not all, whole life policies often come with a savings option. This allows some of your money to accumulate value over the years. This savings option acts as a living benefit, which you can borrow against to make payments during your lifetime, make the most of your insurance policy and relax in the knowledge that your financial future is secure.

What type of life insurance should I buy? Hey there! Figuring out what type of life insurance is right for you can be tough. We’re here to break it down. There are two kinds of life insurance, whole and term. Term insurance covers a specified amount of time. Term policies are generally more affordable and often come with the option to renew or convert to whole life coverage. Term is used for temporary needs, such as protecting your family or covering debt. Whole life insurance covers you for, you guessed it, your whole life. If your interests lie in estate planning or making donations upon your death whole life insurance allows you to plan your finances without renewing or switching policies. So, whatever your situation, the perfect life insurance plan is ready and waiting for you.

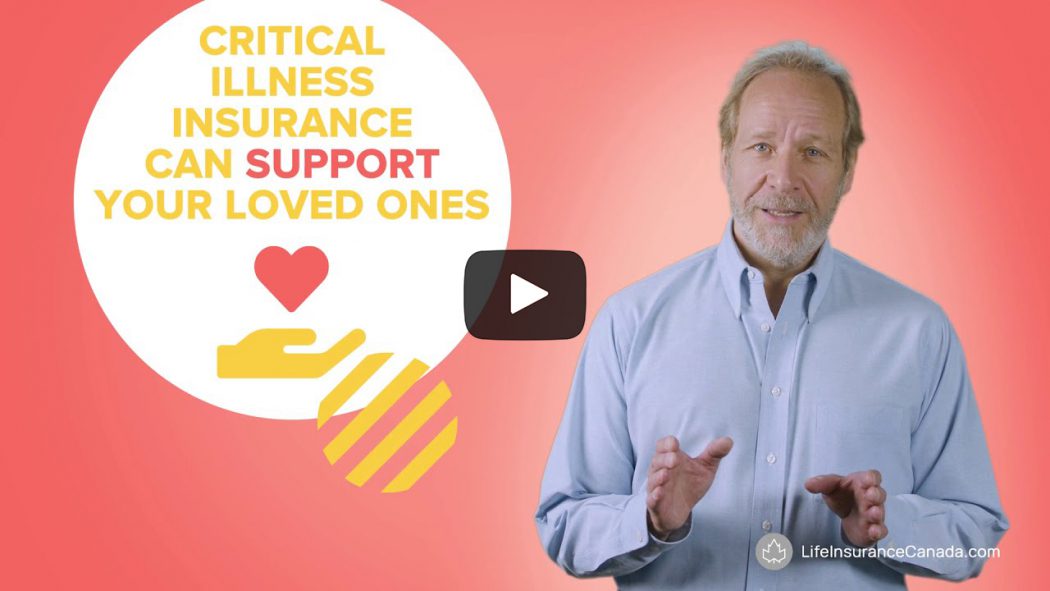

Critical illness, how does it work? A critical illness diagnosis can leave patients and their loved ones struggling to find a sense of control. On top of emotional stress, you might be left with unexpected medical bills. If so, critical illness insurance is here to help. Critical illness coverage pays out a lump sum, tax free, upon your diagnosis. This can be used to cover specialized care, travel expenses or anything your family may need. Leave your financial burdens to your insurance provider, so you can focus on what matters, spending time with the people you love.

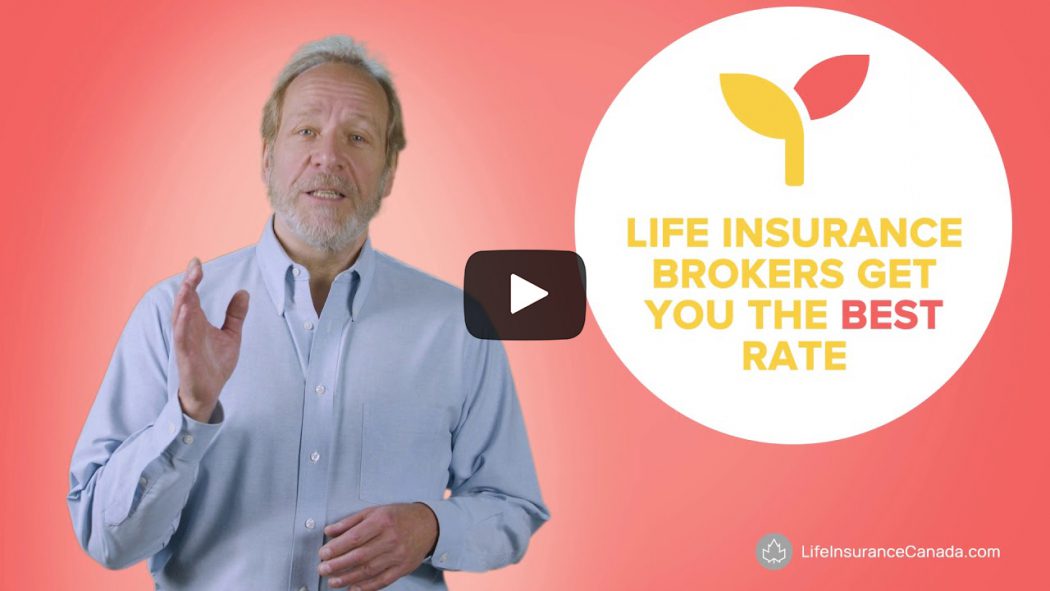

How do life insurance brokers get paid? Life insurance brokers make sure you get the best rate on your policy, but you may wonder how they, themselves, get paid. Most of the money your insurance brokers makes is by commission. Every time they sell an insurance policy, they earn a small percentage of the payments you make. This means that in order to earn a salary an insurance broker must meet all the needs of their client, that’s you. These needs don’t just stop when you begin your payments, brokers will evaluate your policy regularly to advise on any changes and help you submit claims to receive your benefits.

Life insurance as an asset/investment. Planning, your assets and investments is a vital part of your financial future. But many people aren’t aware that life insurance can actually be one of these assets. Cash value life insurance is a whole life plan. Meaning you are covered for your entire lifetime. When you make your monthly payments, your money is split three ways. Some of it goes into death benefits for your beneficiary, some goes directly to your insurer and the rest adds to the cash value. Not only does this cash value grow over time, but you can actually borrow against it to fund payments and investments during your lifetime. Make your insurance policy work for you, with cash value life insurance.

How does COVID-19 affect life insurance? The COVID-19 pandemic has become a significant source of stress in our daily lives. For many of us, this pandemic has made us confront our own mortality. So how is the corona virus going to affect life insurance? If you already have a life insurance policy, you can rest easy. Your policy is designed to cover your death under any circumstances. For first-time buyers, the pandemic has changed the underwriting process. You will be asked if you have had the virus, and if you continue to experience symptoms. Your policy will be evaluated according to any lingering health concerns and insurers may factor in new exclusions. But if no exclusions apply to your new plan, there is no added waiting period. You will be covered and eligible for benefits as soon as your policy begins. Get peace of mind today with life insurance.

Life insurance for diabetics. If you suffer from diabetes, buying standard life insurance can be tricky, but still possible. No medical life insurance is a relatively new product designed to help those with pre-existing medical conditions. No medical life insurance lets you bypass intrusive examinations. You can get coverage online, fast, to protect your dependents from any debt or lost income due to an unexpected death. You can even leave an important legacy by giving a portion of your pay out to a cause or leave gifts for your loved ones. Let no medical life insurance take care of you. No matter your age or medical history.

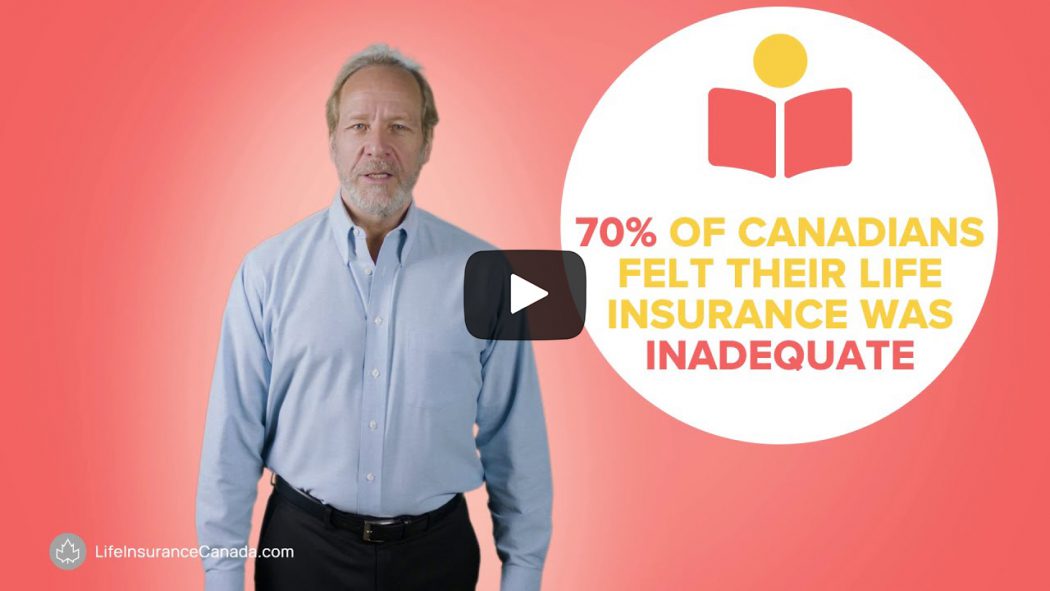

How much life insurance do I need? In 2014 BMO found that more than 70% of Canadians felt that their life insurance coverage was inadequate. So how much life insurance is enough? Your insurance policy is like a great suit, tailored. We’re here to give you a couple of tips to estimate how much coverage you should buy. Life insurance is designed to help with a whole range of expenses. So, it’s recommended that you purchase a policy with seven to ten times your annual salary. Another way to estimate your life insurance needs is to simply multiply your salary by the number of years left to retirement. Bingo. Take control of your financial future and know just how much coverage you need.

How long should my life insurance coverage last? Life insurance can span anywhere from a single year, to your whole lifetime. Figuring out how long your plan should last depends on your situation. The main reasons for purchasing life insurance are to cover your mortgage and protect your dependents in the event of your death. This means you can use your mortgage as a scale. If you intend to pay your mortgage back over a 30 year term, it makes sense to buy a 30 year life insurance policy. You can also factor in the amount of support your family would need following your death. This includes covering your income. If you’re not here, neither is your income. You will want enough coverage to replace your income for your family so they can maintain the standard of living your family is accustomed to. Our licensed advisors can help you determine what policy is right for you and your family.

Life insurance for marijuana users. When marijuana was legalized across Canada, insurers had to adjust the way they see risk. Every company treats marijuana users differently. This is good news and leaves cannabis users with a variety of options, including access to non-smoking rates. The guiding factor for insurers is how often their customer uses cannabis. Some companies do not consider you higher risk unless you use marijuana upwards of four times a week. Others may classify twice weekly consumers as frequent users. While frequency varies from one company to another, occasional marijuana users are never considered higher risk. So, whether you use marijuana daily for recreation, medication, or just while spending time with friends, the perfect life insurance plan is waiting for you.

Life insurance for smokers. Approximately 15% of Canadians smoke cigarettes. Smoking half a pack a day amounts to approximately $2,500 per year. And it’s not just the cigarette that will cost you. Did you know that being a smoker can double your life insurance premium? You might think this increase is limited to tobacco products, but vaping, nicotine gum, patches, and any other smoking cessation products also increase your health risks. Smokers and nicotine users are most likely to experience premature death or critical illness. Insurers take this risk extremely seriously. The more risk you pose to an insurer, the higher your premium. Protect your health and protect your finances with life insurance today.

Life insurance for people with depression/anxiety. Buying life insurance can be daunting at any time, but may seem especially difficult when dealing with a mental illness. Approximately one in five Canadians experience mental illness every year. But how does mental health impact your life insurance? When you purchase a policy, your insurer will ask you a list of questions, including the date of your diagnosis, the severity of your symptoms, how your illness affects your life, and whether you are on medication. The provider estimates your premium based on your answers. If you aren’t sure what kind of policy you need, independent insurance brokers are here to help. Rather than have you purchase directly from a company, independent brokers present a variety of options so you can pick the policy that’s right for you, no matter your situation.

No medical life insurance policies. No matter how complicated your medical history, you deserve great life insurance coverage. But finding life insurance coverage while dealing with a preexisting medical condition can be tough. Thankfully, no medical life insurance is here to make things simple. No medical insurance comes in both term and whole life plans and does not require intrusive medical exams. The simple online underwriting process helps you get fast and affordable plans that suit you. Seamlessly cover funeral expenses, personal debt, and leave a legacy for your loved ones with no medical life insurance.

Still have questions? Search our insurance library for answers.

Search our blog

One of the largest online resources in Canada for life insurance.