Term Life Insurance

Term Life Insurance Permanent Life Insurance

Permanent Life Insurance No Medical Life Insurance Canada

No Medical Life Insurance Canada Critical Illness Insurance

Critical Illness Insurance

Expert Advice from a 15-Year Veteran

As a 15-year veteran of the life insurance industry, I can’t tell you how many times I have heard clients tell me that they wish they had started their insurance program when they were younger. Many people have heard me make the comment over the years that as you age, one thing I know for sure is that you are getting closer to the end of your life. The last time we checked, the mortality rate in Canada was still 100%. This is, of course, a bit tongue-in-cheek, but when you look at it from the perspective of an insurance company, you need to understand that it holds true. As you age, an Insurer knows for sure that every year older you are, you are exactly one year closer to the end of your life. There’s another truth in here as well. The odds that something will end your life are slightly higher every year as well.

What does this mean to you? If you are thinking about applying for life insurance, now is the time to do so. Do you have a family or business that would experience financial hardship if you passed away? Do you have an estate that the tax man is coming for you when you die? Do you want to use the most tax-efficient way of passing wealth from one generation to the next? Apply for life insurance. Do it today. Delaying will only cost you more when the solution has always been available to you.

Read further to get a bit of information on who can apply for life insurance and how to apply for it. There is some interesting information on how when you apply for coverage, it could influence the coverage that you get.

Overview

We are going to address a few key points in this article from the perspective of an advisor who has helped many people apply for life insurance over the years. They include:

- Who Can Apply for Life Insurance

- The Steps in the Process of Applying for Life Insurance

- Why Applying for Life Insurance is Important

- What I Need to Have to Apply for Life Insurance

- The Role, an Insurance Broker, can play in Applying for Life Insurance

Who Can Apply For Life Insurance?

There are many reasons that people will apply for life insurance. One question that gets asked frequently is what, if any, are the most common eligibility requirements I need to meet to apply for life insurance.

Here are a few of the common ones:

- Age: You can apply for life insurance at any time. Starting at age 0 (in most cases, you need to be at least 14 days old and home from the hospital) and, depending on the carrier, potentially as old as when you are 90.

- Health: Obviously insurers prefer you to be in good health when you apply, but underwriting may allow you to get coverage even if you have some issues with your health. There are also guaranteed issues and no-medical policies where you can get coverage regardless of your current health.

- Residency: If you are not a Canadian citizen, you can still apply for life insurance in Canada. You need to be present in the country while you are applying, and most insurers prefer that you have resided in Canada for a few months and have applied for permanent residency in order to have your application considered.

- Income: There is no limit to the income you need to apply for life insurance. However, you should be aware that this can limit the amount of coverage that an insurer will issue. Carriers want to avoid a situation where you are worth significantly more dead than alive, so if you don’t have a lot of debt obligations and the purpose of the policy is purely income replacement, they may limit how much death benefit you can apply for based on how much your current income is.

- Purpose: You can apply for life insurance for many reasons; in Canada, though, there needs to be something called an ‘insurable interest‘ for the policy. This means that there needs to be a financial impact on you or someone close to you for a policy to be issued. I can own a policy for my child, spouse, or business partner because if something happened to them, there would be a direct financial impact on me. I can’t own it on my neighbour, who I happen to know is one of those guys who likes to BASE jump while wearing the flying squirrel suit. I get that it seems like a good investment to own a life insurance policy for someone who has dangerous hobbies, but if something happens to my neighbour, there usually isn’t a financial impact on me.

Steps to Applying for Life Insurance

As a veteran life insurance broker in Canada with 15 years of experience, I am often asked about what is involved in applying for life insurance. Consulting with an experienced advisor can make the process of buying life insurance much easier as they will guide you through it. If you choose to venture forth on your own, here are the steps you should be taking to apply for life insurance from start to finish:

Step 1: Assess Your Needs

- This is the needs analysis portion, and it forms the foundation for all of the planning going forward.

- To begin with, evaluate all of your current financial obligations: You should consider debts, mortgage, education costs, and other financial responsibilities.

- Once you’ve assessed what your financial obligations are you should also consider are they temporary or permanent? Temporary obligations are the ones that go away, like a mortgage, for example. Permanent obligations are things like funeral expenses that will always be there.

Step 2: Research and Choose a Policy Type

- With your needs analysis completed, you can now proceed with figuring out what type of life insurance you are going to apply for. There are two main categories of life insurance policies.

- Term Life Insurance: Offers coverage for a specific period (e.g., 10, 20, 30 years) and is generally more affordable. Term life is ideal for covering the temporary needs that are in your needs analysis.

- Permanent Life Insurance: Provides lifelong coverage and includes options like whole life or universal life policies. This type of coverage is best suited for your permanent needs like estate planning and final expenses.

Step 3: Get Quotes

At this point, you may need to engage with an advisor. The experts at LifeInsuranceCanada.com are familiar with the offerings from many different insurance companies and will help recommend a solution to you from an insurer that excels in your particular situation. They will consider things like:

- The reputation, financial stability, and customer review of the insurer.

- They will be able to request quotes from multiple insurance providers to compare rates and coverage options.

Step 4: Complete the Application

You will need to complete an application with the insurer you choose. You should be ready with the following information as they may request it as part of the application.

- Personal Information: Provide your full name, date of birth, address, and Social Insurance Number (SIN).

- Health Information: Disclose any medical conditions, medications, and lifestyle habits (e.g., smoking, alcohol consumption). They may also ask if you have a family doctor, who it is, if you do when the last time you saw a doctor was and why you visited them.

- Financial Information: Include details about your income, assets, and liabilities.

- Beneficiaries: Specify who will receive the death benefit.

Step 5: Pay the Initial Premium

Assuming you are healthy at the time of application, the insurer can offer you temporary insurance. This establishes the coverage from the time of application as long as you pay the first premium. The insurer is still entitled to underwrite the policy and could potentially offer a modified coverage or decline coverage if they found something during this process. If you are confident that this is unlikely to happen, paying the first premium with the application starts coverage right away.

- Make the first premium payment to activate the policy. This can usually be done via cheque, credit card, or electronic funds transfer (EFT).

- Set up automatic payments if desired to ensure timely payments and avoid lapses in coverage.

Step 6: Undergo a Medical Exam (if required)

Depending on the death benefit you are applying for, you may be required to undergo a medical exam arranged by the insurer. If that is the case, you can expect to provide the following:

- Blood tests

- Urine tests

- A small physical exam.

Note that some policies, like simplified issue or guaranteed issue life insurance, may not require a medical exam but typically come with higher premiums and lower coverage amount.

Step 7: Review the Underwriting Decision

- If the policy is issued as a standard contract you still want to carefully read the policy’s terms and conditions to understand the coverage details, exclusions, and any riders (additional benefits).

- If there are exclusions (i.e. specific things that would result in the policy not paying the death benefit) make sure you understand them. An example would be a good friend of mine has a policy that won’t pay off if he dies as a result of a skydiving accident. He was fine to accept that exclusion because he no longer skydives, but he had done it recently before applying for life insurance so the company excluded that cause of death.

- Confirm that the policy meets your needs and expectations.

Step 8: Receive the Policy Documents

- After approval, the insurance company will send you the policy documents. Review these documents to ensure all information is accurate and that the coverage matches what was agreed upon.

- There will be a period of time called the ‘free look .’This is a window of 10 – 30 days (depending on the insurer) where you can review the coverage and return it for a refund of premiums paid if there’s something you don’t like with the policy terms and conditions.

- Keep the policy documents in a safe place and inform your beneficiaries about the policy and its location.

Step 9: Regularly Review and Update Your Policy

- Periodically review your life insurance policy to ensure it continues to meet your needs. Remember that the needs analysis when you set the plan up reflects your situation at that exact time in your life. As time passes, your needs may change as well.

- Update the policy if there are significant life changes, such as marriage, the birth of a child, or a change in financial situation.

Step 10: Communicate with Your Beneficiaries

- Make sure your beneficiaries know about the policy and understand how to claim the benefits.

- Provide them with the necessary contact information for the insurance company.

Download Your Checklist for Applying for Life Insurance

The Importance of Applying for Life Insurance Early

Life insurance is truly one of the products that you lose out on by delaying applying for it. There are two main reasons for this. The first is that the premium calculation is based on how old you are on the day that you apply. The older you are, the more expensive the policy will be. The second factor is your health. No one knows what tomorrow holds, and unexpected changes in your health can make applying for life insurance much more costly. Check out the 2024 Insurance Barometer Study for more thoughts on the importance of applying for life insurance. The study shows that many consumers recognize the financial advantages of purchasing life insurance early in life. Source: LIMRA (https://www.limra.com/barometer)

Applying for life insurance early in life can provide you with:

- Cheaper Rates: Younger applicants have lower premiums because the older you are, the closer you are to the end of your life.

- Guaranteed coverage: Applying early can secure coverage before any health issues. If your health changes after your life insurance is in place the insurer is not allowed to change the terms of the policy.

- Immediate Protection: Early application ensures immediate protection. This means that if something unexpected happens today, you will be covered because you applied for life insurance yesterday.

- Long-term savings: Whole and universal life insurance policies accumulate cash value, so if you enter into a policy like this when you are young, these values have many years to accumulate.

- Peace of Mind: Applying for life insurance early provides you with the peace of mind of knowing that if something happens to you your beneficiaries will be looked after financially.

2024 Insurance Barometer Study The study shows that many consumers recognize the financial advantages of purchasing life insurance early in life

Source: LIMRA (https://www.limra.com/barometer)

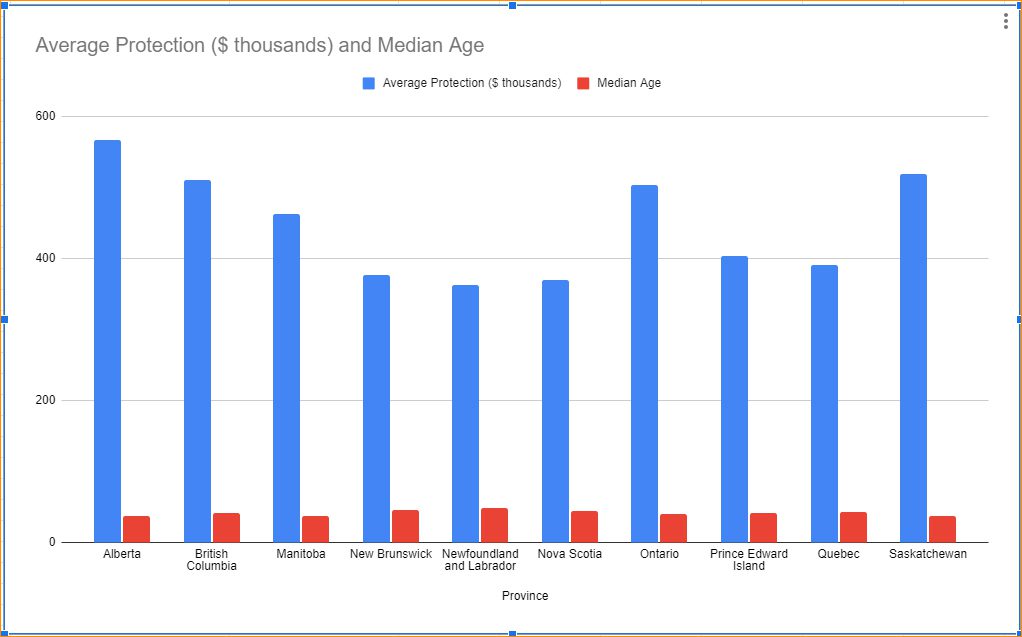

Life Insurance Protection & Age Breakdown by Province

This table summarizes the average life insurance protection per insured household and the median age of policyholders across different provinces in Canada. Here is a table that summarizes the distribution of life insurance policies, and their owners, across Canada It summarizes the average life insurance protection per insured household and the median age of policyholders across different provinces in Canada. The values are reflective of the protection coverage based on the policyholders’ age, income levels, marital status, mortgage balances, and target income for dependent support.

Table: Life Insurance Protection and Age Breakdown by Province

| Country/Province | Average Protection per Insured Household ($ thousands) | Median Age |

|---|---|---|

| 567 | 38 | |

| 511 | 42 | |

| 462 | 38 | |

| 363 | 48 | |

| 377 | 46 | |

| 370 | 44 | |

| 504 | 40 | |

| 404 | 42 | |

| 391 | 43 | |

| 519 | 38 |

Chart of Life Insurance Protection and Age Breakdown by Canadian Province

Here is another chart showing the median age of life insurance policy owners and the average amount of coverage that they have in the different provinces in Canada.

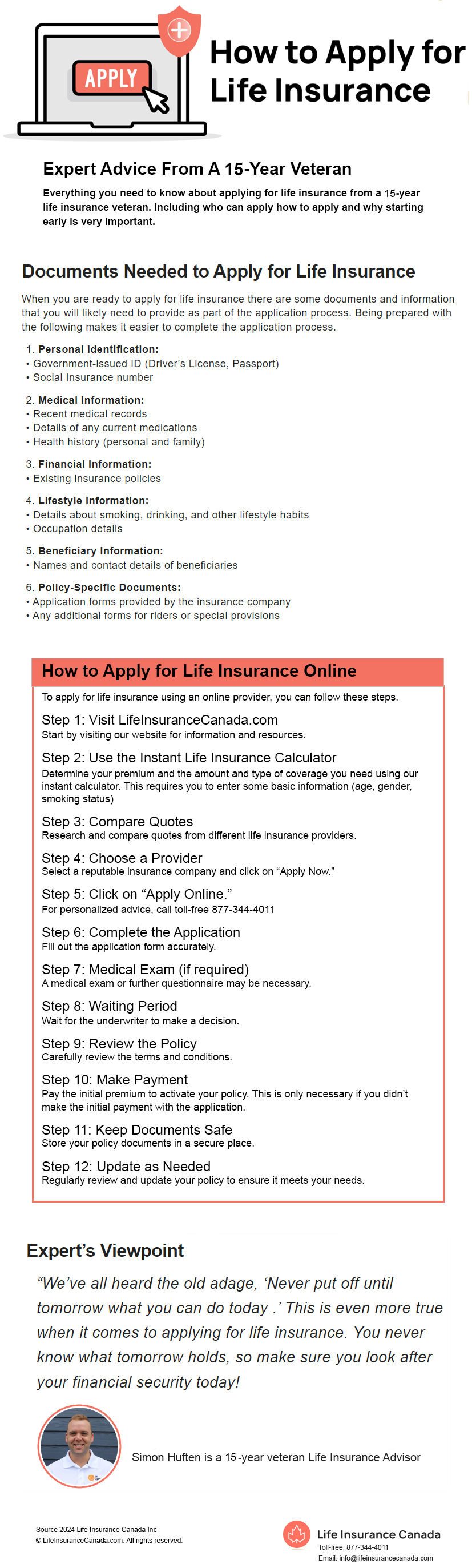

Expert’s Viewpoint

We’ve all heard the old adage, ‘Never put off until tomorrow what you can do today .’ This is even more true when it comes to applying for life insurance. You never know what tomorrow holds, so make sure you look after your financial security today!

Simon Huften is a 15-year veteran Life Insurance Advisor

Simon Huften is a 15-year veteran Life Insurance Advisor

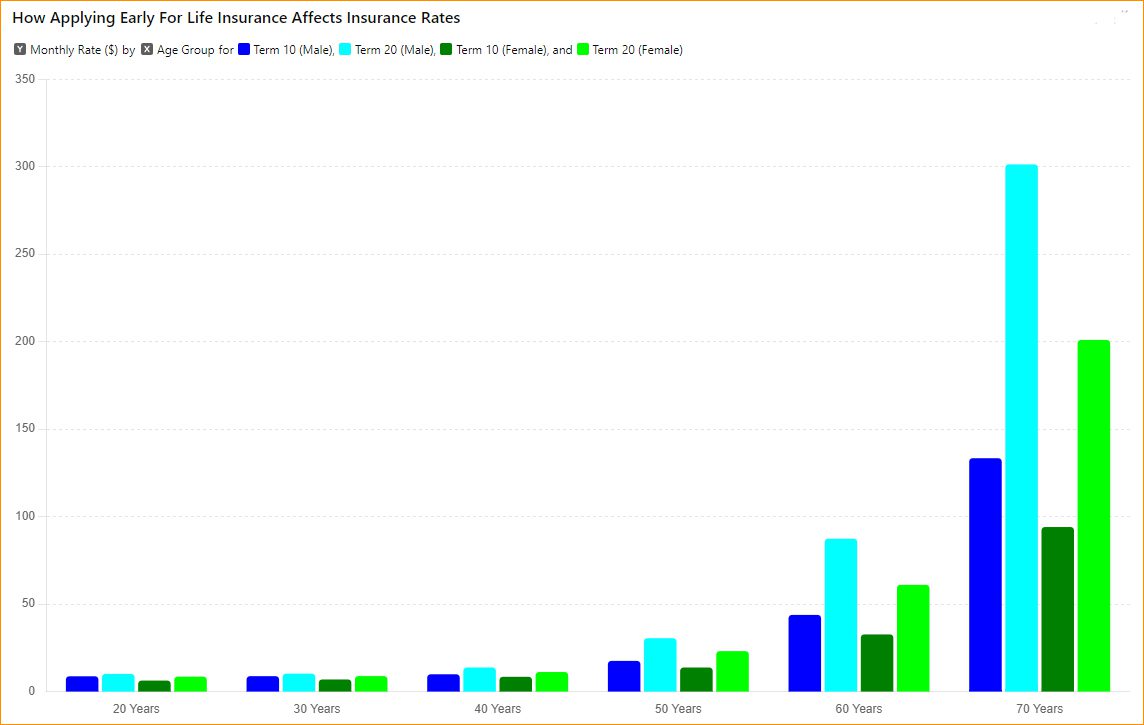

Simon Huften is a 15-year veteran Life Insurance AdvisorTable: Term Rates When You Apply for Life Insurance Early

Here is a table that shows an example of the cost of delaying applying for life insurance. As you can see, even if you remain healthy, waiting to apply for life insurance costs more every year simply because you are older.

(Regular rates, non-smoker)

| Age Group | Coverage Amount | Term 10 (Male) | Term 20 (Male) | Term 10 (Female) | Term 20 (Female) |

|---|---|---|---|---|---|

| 20 Years | $100,000 | $8.75 – $18.00/month | $10.08 – $19.71/month | $6.30 – $10.71/month | $8.55 – $12.24/month |

| 30 Years | $100,000 | $8.82 – $18.81/month | $10.26 – $20.34/month | $6.93 – $11.07/month | $8.87 – $13.50/month |

| 40 Years | $100,000 | $9.90 – $21.69/month | $13.77 – $23.67/month | $8.46 – $17.19/month | $11.19 – $20.61/month |

| 50 Years | $100,000 | $17.55 – $35.64/month | $30.51 – $53.91/month | $13.77 – $30.15/month | $23.13 – $39.51/month |

| 60 Years | $100,000 | $43.83 – $87.66/month | $87.39 – $137.52/month | $32.67 – $67.59/month | $61.02 – $92.07/month |

| 70 Years | $100,000 | $133.38 – $304.29/month | $301.32 – $438.30/month | $94.05 – $192.51/month | $200.97 – $300.51/month |

Bar Chart: How Applying Early For Life Insurance Affects Insurance Rates

The following chart really shows the value of applying for life insurance early. It shows the monthly insurance rates for Term 10 and Term 20 life insurance policies for males and females across different age groups (20, 30, 40, 50, 60 and 70 years old). Here are the key observations and insights:

Key Observations:

- Trend of Increasing Rates with Age:

• The chart clearly shows that insurance rates increase significantly with age for both Term 10 and Term 20 policies. What you also see is that the increase isn’t linear. Again, this is reflective of the fact that the older you are when you apply for life insurance, the higher the risk is to the insurer. - Gender Comparison:

• For both Term 10 and Term 20 policies, females generally have lower insurance rates compared to males. This difference reflects the fact that historically females have a longer life expectancy than males and as such the risk to the insurer is lower. - Comparison Between Term 10 and Term 20 Policies:

• As expected, Term 20 policies have higher rates compared to Term 10 policies for both genders and across all age groups. Although this is the case when the policies are issued you need to consider how long the need you are covering is because over 20 years it may be more cost effective to take the 20 year option from day one as opposed to a ten year policy that renews at a higher premium for years 10-20. - Impact of Applying Early:

• The clearest example of this is that the younger you are when you apply, the lower the premium you will pay. For example, a 20-year-old male pays between $8.75 – $18.00/month for a Term 10 policy, while a 70-year-old male pays between $133.38 – $304.29/month for the same coverage. Similarly, a 20-year-old female pays between $8.55 – $12.24/month for a Term 10 policy, while a 70-year-old female pays between $94.05 – $192.51/month. Obviously, the risk is much higher to insure a 70-year-old than it is for a 20-year-old.

Documents Needed to Apply for Life Insurance

When you are ready to apply for life insurance there are some documents and information that you will likely need to provide as part of the application process. Being prepared with the following makes it easier to complete the application process.

- Personal Identification:

• Government-issued ID (Driver’s License, Passport)

• Social Insurance number - Medical Information:

• Recent medical records

• Details of any current medications

• Health history (personal and family) - Financial Information:

• Existing insurance policies - Lifestyle Information:

• Details about smoking, drinking, and other lifestyle habits

• Occupation details - Beneficiary Information:

• Names and contact details of beneficiaries - Policy-Specific Documents:

• Application forms provided by the insurance company

• Any additional forms for riders or special provisions

Understanding the Underwriting Process

Once you have completed your application, it will be submitted to the underwriting department of the insurance company with which you have applied for coverage. This is the insurer’s opportunity to assess the risk you pose based on the information you provided. If they have requested any medical tests (blood work, for example), they will also factor these results into their process. Using all of the information they collect, the insurer has a few options:

- They can issue the policy as applied, typically known as a ‘standard’ policy.

- They can request extra premiums to offset a higher-than-normal risk. This is known as ‘rating’ a policy. The policy covers you fully but you pay extra for it because of something in the health or lifestyle information you provided.

- They can issue the policy with a lower premium than originally quoted. These policies are referred to as ‘preferred’ rates, and they are offered to applicants with spotless health, lifestyle and family histories to reflect that they are better risks for the insurer.

- The policy could be issued as a standard but with exclusions. This would be regular premiums but there could be specific things that aren’t covered if they are the cause of death. Im looking at you flying squirrel-suit wearing, BASE jumping guy.

How Much Life Insurance Do I Need to Apply?

This is where you need to make use of a needs calculator and enter your financial obligations into the calculation. The main thing to remember here is that you need to calculate based on the idea that if something happened to you yesterday, what would your beneficiaries need today? Since you are planning for an unknown event, you can’t take the chance to guess the future. If your mortgage is going to be paid off in 10 years, you can’t plan today as if it has already been paid. That type of thinking can create a shortfall if something unexpected happens.

Insurance Needs Calculator

What Will Life Insurance Cost Me?

How to Apply for Life Insurance Online

To apply for life insurance using an online provider, you can follow these steps.

Step 1: Visit LifeInsuranceCanada.com

Start by visiting our website for information and resources.

Step 2: Use the Instant Life Insurance Calculator

Determine your premium and the amount and type of coverage you need using our instant calculator. This requires you to enter some basic information (age, gender, smoking status)

Step 3: Compare Quotes

Research and compare quotes from different life insurance providers.

Step 4: Choose a Provider

Select a reputable insurance company and click on “Apply Now.”

Step 5: Click on “Apply Online.”

For personalized advice, call toll-free 877-344-4011

Step 6: Complete the Application

Fill out the application form accurately.

Step 7: Medical Exam (if required)

A medical exam or further questionnaire may be necessary.

Step 8: Waiting Period

Wait for the underwriter to make a decision.

Step 9: Review the Policy

Carefully review the terms and conditions.

Step 10: Make Payment

Pay the initial premium to activate your policy. This is only necessary if you didn’t make the initial payment with the application.

Step 11: Keep Documents Safe

Store your policy documents in a secure place.

Step 12: Update as Needed

Regularly review and update your policy to ensure it meets your needs.

What our clients are saying about LifeInsuranceCanada.com

Maggie McCarthy

“I applied online and I received a written response to the quote. On the same day, I spoke with representative, James Duncan, who was knowledgeable and answered all my questions. He, in turn, had Natasha Smith contact me and she handled all the necessary actions to turn the application for a life insurance policy to an active policy, with a reputable company, for a reasonable premium. Top drawer experience.”

Source: https://maps.app.goo.gl/weoZWQxgTUa612oB7

Wendy Lewis

“Was a relatively easy process to apply for life insurance and compare to a lot of different companies to chose the one that best fit our needs.”

Source: https://maps.app.goo.gl/cnNoyfiaCd6FZkLY7

Remember, When You Apply for Life Insurance

To make sure that when you apply for life insurance, it goes smoothly, you need to follow one simple concept.

- Be truthful with your answers. This is one of the most important parts of the application. If you answer no to the smoking question, but are in fact a smoker, you have committed fraud on the application and the insurer can cancel the policy at the time of your death because of this. Don’t risk it. Answer all questions truthfully.

- Be truthful with yourself as well. When you are applying for life insurance make sure that you have taken the time to honestly assess how much you need. This will allow you more peace of mind knowing that your beneficiaries will be taken care of if the worst case scenario happens.

How to Apply for Life Insurance with Pre-existing Conditions

If you have pre-existing medical conditions, it doesn’t preclude you from applying for life insurance. There are many different stories out there of people who have been turned down for life insurance based on pre-existing medical conditions. An example of this was covered by CBC News a few years ago, and you can read about it here. The story in the CBC article doesn’t have the best outcome, but there are things that could have been done to help this family get the life insurance that they needed. If you have pre-existing medical conditions, a couple of factors will become more important when you apply for life insurance.

The first is that you simply must disclose all of the details about your preexisting condition on the insurance application. Again, any attempt to mislead the insurer, even by omission, can be treated as fraud and could result in the cancellation of your policy in the future, even at the time of claim. This means that your death claim could be denied if the insurer finds out that you had a medical condition that would have influenced their decision on coverage.

The second factor is that working with an expert like the advisors at LifeInsuranceCanada.com can really help. Different insurers view medical and lifestyle items differently from one another. This means that while one carrier may decline to cover you based on a pre-existing condition, a different insurer may be willing to take on the risk. When you are applying for life insurance, having someone to guide you to which company will work best with your particular situation can make the whole process less frustrating. In the example from the CBC story, perhaps there was a carrier other than the one company that they applied with that would have been able to issue the policy for this family. One of the big advantages of dealing with a company like LifeInsuranceCanada.com is that they have partnerships with many different insurers and are more likely to be able to find a solution for you because of this.

A Story from One of Our Clients

In a review of her interaction with LifeInsuranceCanada.com Ma. Blesilda Mendoza posted that she was “Very satisfied with the service. They will keep you informed and updated on the status of your application. Will definitely reach out to them again if needed.”

She then added an update to her story. “Also applied for my husband (as he has been denied before with other insurance brokers), but Life Insurance Canada were able to find an insurance company and have his application approved. Very satisfied.”

This is a client who experienced firsthand the power of dealing with a company like LifeInsuranceCanada.com when applying for life insurance. Having had her husband denied coverage before was a frustrating experience because they obviously recognized the value of having life insurance and were applying for life insurance to offer financial security for their loved ones if they were to pass away. When you recognize the value of insurance, being told you can’t have it is a tough pill to swallow. Unfortunately, many people think that they are out of options when told once that they can’t have insurance. This isn’t the case and LifeInsuranceCanada.com’s team was able to provide the coverage that the family wanted when they had been told no elsewhere.

Insurance Broker’s Role in the Application Process

The insurance landscape in Canada is complicated. There are more than thirty different companies issuing life insurance in Canada in 2024. The role of the broker when you apply for life insurance is to guide you through this crowded mess and help you land with the best provider for your individual needs. They also should work with you to make sense of the decision between term insurance and permanent insurance and help you land the proper mixture of those products for your individual situation.

Think of it this way. Throughout our daily lives, we work with experts in all kinds of fields. If your car breaks down, you take it to a mechanic; if you want to go on vacation, you seek out a travel agent or travel web service. In all likelihood, you are an expert at your job, and others seek out advice from you. This is because it is impossible for one person to know everything about everything. When you apply for life insurance, your broker’s role is to be the expert. You tell them what you need, and they find the solution that works best for your unique situation.

FAQs

Q: What age can you apply for life insurance?

A: You can apply from age 0 to age 90. Just remember that the younger you are when you apply, the better your premiums will be.

Q: What happens if you don’t disclose information when applying for life insurance?

A: Your policy is at risk. This constitutes committing fraud on your application, and when the insurer finds out, they can cancel your policy, even if they happen to find out at the time that you have died.

Q: Can I apply for life insurance for someone else?

A: You can, as long as there is a financial consequence to them passing away that affects you directly. So your kids, your spouse, and your business partner are all examples of someone else you could own life insurance on.

Q: Can I apply for multiple life insurance policies?

A: Yes, you can apply for multiple policies, even at the same time. You should take care, though, that it doesn’t look like you’re trying to get a lot of coverage all at once but want to avoid needing to go through the more in-depth underwriting one large policy would require. Someone applying for $1 million in death benefit by getting ten $100,000 policies all at the same time could send up a flare as to why they aren’t simply getting one policy for what they need from one place.

Infographic: How To Apply For Life Insurance

Final Thoughts

After many years in the insurance industry, I can say with full confidence that the time to apply for life insurance is now. If you have people who rely on you for financial support, you should not wait another day. If you wait, you run the risk of a change in your health or the fact that you have gotten older, making what you need unaffordable. Insurance is something you need to get before you need it. I like to use the example of fire insurance for your home. It needs to be in place before your kitchen is on fire. If you call after the fire starts and ask for a policy, you’re really unlikely to get what you need. Applying for life insurance is the same idea; if you’ve waited until your health has changed and your death looks more imminent, you will not be able to get coverage. You need to get it before your health changes.

Take the First Step Now!

Apply for life insurance now. The peace of mind of knowing that if something unexpected happens to you, your family or your business is taken care of financially is not worth taking the chance of waiting. Reach out to the experts at LifeInsuranceCanada.com to help guide you through applying for life insurance. We will make sure that you land with the best coverage for your unique situation.

Get a free quote

LifeInsuranceCanada.com has Over 200 Five-Star Google Reviews!