Term Life Insurance

Term Life Insurance Permanent Life Insurance

Permanent Life Insurance No Medical Life Insurance Canada

No Medical Life Insurance Canada Critical Illness Insurance

Critical Illness Insurance

Uncover the truth about whole life insurance and why many Canadians call it a scam, how it really works and when it can still make sense for your goals.

Quick Answer

No, whole life insurance is not a scam but for most people, it’s a poor investment.

It’s built for long-term estate planning, tax sheltering, or high-net-worth individuals, not for everyday savers.

If your main goal is to protect your family or replace income, term life insurance is the smarter, cheaper choice.

Should you buy whole life insurance? Buy whole life if you’ve already maxed out your RRSP and TFSA and want a tax-efficient way to leave money to your heirs.

Otherwise: Buy term insurance and invest the difference.

On This Page

- Why So Many People on Reddit Call Whole Life Insurance a Scam

- Introduction — Why People Call It a “Scam”

- Myth vs Fact

- What Whole Life Insurance Actually Is

- How Whole Life Differs from Term Life

- Why Whole Life Insurance Costs More

Show full table of contents

- The “Forced Savings” Argument — Pros and Cons

- Cash Value: What It Is and What It Isn’t

- When Whole Life Works (and for Whom)

- Whole Life Insurance — Assessment

- When It Doesn’t Work

- Case Study: Term Life + Investing the Difference

- The Tax Shelter Angle

- Why Some Advisors Push Whole Life Too Hard

- How to Spot Red Flags in a Sales Pitch

- Expert Opinion

- How to Decide if Whole Life is Right For You

- Alternatives to Consider Before Buying

- FAQ

- Key Takeaway

- Conclusion & Final Verdict

Why So Many People on Reddit Call Whole Life Insurance a Scam

Let’s get one thing clear from the very beginning here. The internet has been a great tool for many things since its introduction to society. It has made communicating with people easier, made many business transactions easier to complete and given us access to educational resources that never would have been possible in the days of the World Book Encyclopedia.

There are also significant issues that have arisen from the internet playing such a large role in our lives. One of the biggest issues is the rise of the online forum, where someone can ask a question and anyone can answer, regardless of whether or not the person offering the answer actually knows what they are talking about or they are simply providing their opinions as fact.

Reddit is a site where the content is user generated and not fact checked at all. The users adding information can do so anonymously and the more extreme the opinion, the more often it seems to get ‘up votes’ making it more visible for others to read in the thread.

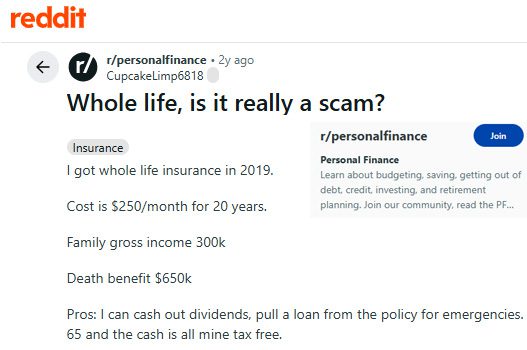

Consider a common Reddit thread where a Redditor asks if he was scammed when he bought a whole life insurance policy. The author signed up for a whole life insurance policy back in 2019 and paid $250 a month for it. After 5 years the cash value was less than the amount that had been paid in premiums and the dividends that had accumulated in the policy didn’t make up the difference. The owner now feels like he may have been sold an investment product called a ‘Super ROTH’ which is similar for Americans to the Canadian RRSP or TFSA. The owner wonders if he was scammed. Let’s take a look at this and figure that out.

He signed up for whole life insurance back in 2019, paying $250/month for 20 years. After 5 years, he had poured in $15,000, yet the cash value was only about $11,500 and the “dividends” he could take out barely justified the cost.

Now in his early 50s, he’s questioning whether he was sold a “super-Roth” (the U.S. equivalent of a Canadian TFSA or RRSP) or a disguised scam. He admits:

“The only downside I see is if the cash value exceeds the death benefit… the family gets $650K, but the company keeps the rest.”

That story captures exactly why so many people online are debating whether whole life insurance is a scam?

To understand the arguments on both sides and when it makes sense, or doesn’t, let’s begin with the fundamentals.

Source & Attribution

This real story first appeared in a public post on Reddit.¹

¹ “Whole life, is it really a scam?” Reddit, r/personalfinance.

Reviewed by Simon Huften, President of LifeInsuranceCanada.com a licensed Canadian life insurance advisor with over 15 years of experience.

1. Introduction — Why People Are Asking if Whole Life Insurance Is a Scam

The Online Debate

As I mentioned earlier, the internet has given us many wonderful things. Where else can you sit and watch endless hours of funny cat videos or find out what the name of that actor that you recognize in that show you’re watching is instantly?

It has also led to some less wonderful things though, I would include in this list the idea of allowing everyone a voice, even on topics that they really don’t have the expertise on to be providing ‘help’ to people who are asking questions.

I am constantly telling my children that they need to understand their sources when it comes to information that they spout like facts and that perhaps their favourite YouTuber or TikTok poster aren’t the world’s most reliable sources.

YouTube in particular has reel upon reel of ‘experts’ who offer their opinions on why whole life insurance is a scam. They consistently come back to the fact that your insurance advisor makes more money when they sell you a whole life policy than they do with other products.

As a side note, if the video you’re watching simply says that under no circumstance should you buy whole life insurance then rest assured you’re watching the wrong video to get your answer. You should see someone who, while they offer their opinion they also recommend that you seek out advice on your personal situation. If it is a blanket ‘no way’ to whole life insurance there is often another agenda for the person posting that content.

When you begin a Google search with the phrase ‘Is whole life insurance’ the guesses that Google makes as to how you want to finish questions include ‘worth it’, ‘a good investment’, ‘taxable’ and ‘a good idea’.

Out of all of these questions only one of them has an empirical answer that applies to all policies. That is the question about its tax treatment. There are rules laid out as to when and how life insurance values are taxed and this question can be answered from facts you would find from a Google search.

The other questions…. they aren’t so simple to answer because there is no black and white set of rules as to who whole life insurance is appropriate for and who it isn’t.

This is why working with an advisor that understands your unique situation and makes recommendations to you based on those circumstances is so important. Whole life insurance is not a scam, it is a legitimate and powerful financial planning tool that, when applied in the proper situation, can make incredible differences in the life of the policy owner and their beneficiaries.

Just How Many Canadians Have Life Insurance?

Here’s why I am writing this article on whether or not whole life insurance is a scam. My goal is to provide you with facts and to encourage you to remember that there is no answer to the question ‘is whole life insurance a scam’ that applies to everyone. Whole life insurance will fit with some people’s needs and not with others. What we do know for sure is that there are millions of Canadians who rely on life insurance to protect their families. According to the Canadian Life and Health Insurance Association (CHLIA) in a study published in 2025 there was nearly $143 billion paid in benefits from Canadian insurance companies that helped to protect nearly 30 million Canadians in 2024. With this data showing just how valuable Canadians find life insurance we will try to separate fact from myth over if whole life insurance is a scam or not.

Here is the data from the CHLIA on Canadians with life insurance:

| Metric | 2024-2025 | Source |

| Canadians with life insurance | 23 million | CLHIA 2025 Facts p. 13 |

| Total coverage | $6 trillion | CLHIA 2025 Facts p. 13 |

| Average household coverage | $509,000 | CLHIA 2025 Facts p. 14 |

| Life insurance benefits paid | $18.6 billion | CLHIA 2025 Facts p. 8 |

| Total benefits (life + health + retirement) | $413 billion | CLHIA 2025 Facts p. 8 |

Source: CLHIA 2025 Facts Report – pp. 8–13

2. Why People Call It a “Scam”

Why Even Some Canadians Think Whole Life Is a “Scam”

When it comes to the discussion of why people seem to think that whole life insurance is a scam we really need to determine what the issue that they have is. Do they feel like the product itself is a scam or is it the process by which they were sold the product that they feel scammed them?

My suggestion would be that far more often it is the process and not the product that leaves people feeling like they were scammed. Unfortunately this is true of most things in life. There are people out there who take advantage of their position as perceived experts on topics that will take advantage of those people with less knowledge for their own benefit.

And yes, it is true that selling a whole life insurance policy often results in a higher amount of commission being paid to the seller. (As a side note, the wording in that statement is important. The amount of commission is higher. This is because life insurance companies pay commission based on the premium that the policy carries. Whole life insurance has a higher premium than a term policy does so in the end the commission is higher, but it isn’t because you sold a whole life policy, it is because of the premium amount. If you sold a term policy with a large premium attached to it the commission would also be high.)

This becomes the main focus of the internet conversation. Over and over online the story is ‘look at how much money they earn by selling me a whole life insurance plan’. It must be a scam that the sales people push because they make more money from it.

Too often the life insurance broker or agent selling the policy in a situation where the buyer ends up feeling like they were scammed focused on the wrong things. With the case of the angry Redditor mentioned earlier, the focus was on the cash value in the policy and not the life insurance death benefit.

If you buy whole life insurance for any other reason than the death benefit then you may end up feeling like these insurance policies are a scam.

But if you focus on the true use of life insurance, which is to provide your beneficiaries with an infusion of cash, paid tax-free to them when they need it most, you quickly see that when used properly whole life insurance is far from a scam.

When you look at the data about life insurance in Canada what you see is that the majority of Canadian life insurance premium dollars pay whole life insurance premiums every year. Even as critics question its value, whole life still dominates 68% of total life insurance premiums in Canada, showing just how profitable it remains for insurers. This is supported by data from the Life Insurance Marketing and Research Association (LIMRA) published in 2025.

Key Data (LIMRA, Q2 2025)

| Insurance Product | Annualized Premium Growth | Policy Change | Market Share |

| Whole Life | +6% | -2% | 68% |

| Term Life | +2% | +2% | 19% |

| Universal Life | +5% | =0% | 13% |

Source: LIMRA, Second Quarter 2025 Canadian Life Insurance Sales Report

Common Complaints

What you will see if you follow the trail down the Google path and start to look at why people feel like whole life insurance is a scam is that there are really common themes in the people posting complaints about whole life insurance. A few of these common themes are:

- High upfront costs – When a policy is new there are fixed costs associated with setting it up and building the reserves to offset future risk. The majority of these costs apply early in the life of the policy so there are higher upfront administration costs to establish the policy.

- Slow cash value growth – The bottom line is that whole life insurance is an insurance policy, not an investment plan. So while yes, there is cash value that grows within the policy it is not designed to replicate stock market portfolios. If you want an investment plan, choose an investment plan, not an insurance policy

- High commissions – The commissions earned by life insurance sales people reflect the premium that the policy carries. This is true with all types of policies. This is one of the most common complaints online about whole life insurance is that people complain that a sales person pushed them into whole life insurance because they would make more money from it. If you feel like your advisor is doing this then you need to walk away and find someone else to help you. In situations where a competent advisor is recommending whole life insurance to a client it is because they have a more advanced need (think part of an overall estate plan) and the advisor needs to do more work to find the right solution. If your life insurance advisor is doing the right work for you, the fact that they receive higher commissions for whole life insurance shouldn’t be a concern to you because you are receiving value and they are being compensated for the high level planning work that they are providing.

- Complex illustrations – Whole life insurance can include things like dividend options, policy riders and other features that can make reading the illustrations complicated. Remember that the illustration is a forecast of what the policy could look like in the future given specific growth forecasts and that these values aren’t guaranteed. And make sure that you conduct regular reviews of your policy with your advisor and they are explaining the illustrations to you in language that you understand.

- Low flexibility – Whole life insurance policies have a major advantage in estate planning for Canadians. That advantage is that the death benefit is paid out tax-free to the beneficiaries (this is true of all life insurance policies, not only whole life ones). What this means is that there are rules established by government regulators that prevent people from using life insurance as a method to evade paying income taxes. In order to maintain that tax free status the policy must follow the guidelines from the government, this is why there isn’t the same flexibility as there is in your investment plans.

Sources:

LIMRA (2025) – Canadian Life Insurance Sales Report (Q2 Data)

CLHIA (2025) – Facts Report, pp. 10-13 (industry growth and payouts)

The Psychology Behind the “Scam” Label

People feel like they’ve been scammed when they are buying whole life insurance for a number of reasons. This would include the fact that even though you understand at the time of purchasing a policy that it is for your beneficiaries, after paying the premium for a few months you start to look at it as an expense that doesn’t benefit you at all, so why are you paying it? Combine this feeling with the fact that in many cases people don’t really understand life insurance. As was mentioned earlier, the illustrations can be complicated and there is a lot of industry jargon that, while the advisor is sitting with you makes perfect sense, but when you try to remember what everything means in a week or two it’s confusing. Add to this the reality that there are some less scrupulous life insurance agents that will focus on making the highest commission rather than making sure that the policy fits the needs of the buyers and you can see where the idea that people feel scammed sometimes after the life insurance buying process. Let’s look at some of the reasons people feel scammed:

Often people who feel like they’ve been scammed mention that they believed that they had bought an insurance policy that is also an investment. This is one of the most common problems with understanding whole life insurance because it does have a cash value component, it may be eligible for dividends from the insurance company and you will see that cash value grow every year. The key thing to remember is that whole life insurance is not an investment plan. It is designed to operate as a life insurance policy and will never be able to provide you with the flexibility and potential for high returns that many people expect from their investment plans.

3. Myth vs Fact

As is always the case you will encounter all kinds of myths when you look into if whole life insurance is a scam online. It seems like this would be a good place to take some of the more common myths you will find and explain why they fall into the ‘myth’ category by revealing the facts that discount them.

| Myth | Fact |

| Whole life insurance is a scam. | Whole life insurance is a valuable tool for many Canadians financial security plans. It offers exactly what the name implies, life insurance coverage for your whole life. People who feel scammed often try to use it as an investment account or some other unintended method of use. |

| Whole life earns 6-8% per year. | There are guaranteed increases in the cash values in whole life insurance every year, but as far as what they will be in terms of annual growth you need to refer to your original contract. |

| You lose money if you cancel. | You pay your life insurance premium to protect your beneficiaries in the event that you pass away. If you cancel your whole life policy you may not receive back all of the money you have paid as premiums, but that reflects the cost of the insurance. You haven’t lost money, you’ve paid for insurance coverage. |

| Term life insurance is always better | Term life insurance has a set of needs it fills very well. It doesn’t work for things like estate planning though because you can outlive a term insurance plan because they have built in expiry dates. If you need coverage that will last your whole life, not just until you reach the expiry age, term insurance is not the choice for you. |

Advisor Tip: There is no simple answer to what is the best life insurance for you because everyone has a unique set of circumstances. We need to fit the type of policy you have to your situation.

4. What Whole Life Insurance Actually Is

Whoever named Whole Life Insurance wasn’t aiming for nuance. This is a product that provides you with protection for your entire life. Hence the name, whole life insurance. This is a key difference from term insurance. Term life insurance policies have an expiry date attached to them. That means that you could outlive a term insurance plan. Typically in Canada you will find term life insurance coverage doesn’t extend beyond age 85, so unless you know for sure that you are going to die prior to that age you could outlive the policy. Another key difference from term life insurance is that whole life policies have a level premium for the entire contract. Term policies will include renewal points where the premium will go up as you age. This often makes them unaffordable as the policy owner ages to the point where they are approaching life expectancy (about age 80-84 currently depending on your gender). Whole life insurance with its level premium may cost you more early on in the policy but the fact that the cost stays level for the entire life of the policy makes it much more affordable as you age compared to term insurance. Whole life insurance has three core components:

- Lifetime Protection: The death benefit will pay to beneficiaries because the policy has no expiry date. If you pass away at age 97 or three weeks after you take out the policy your beneficiaries receive the death benefit payment.

- Guaranteed Premiums: The premium for whole life insurance is calculated at the time the plan is issued and doesn’t change for the life of the policy. This makes the coverage significantly more affordable as you age compared with term insurance as it passes through renewal points.

- Cash Value Growth: The cash value that accumulates in the policy from a portion of the premium each year builds in the policy cash value. This is a tax-deferred growth that offers some guarantees about how much the minimum increase will be.

5. How Whole Life Differs from Term Life Insurance

Comparison Term vs Whole Life

| Feature | Term Life Insurance | Whole Life Insurance |

| Coverage Length | Fixed term (10 – 30 years) | Lifetime (permanent) |

| Premiums | Lower initially, increase on renewal | Fixed for life |

| Cash Value | None | Builds over time, tax-deferred |

| Purpose | Temporary protection | Long-term wealth and estate planning |

| Flexibility | Can expire or be renewed | Permanent until cancelled or paid up |

| Cost | 5–10× cheaper than whole life for same death benefit | 5–10× more expensive due to savings component |

| Best For | Income replacement, mortgage, family protection | Estate planning, tax sheltering, business succession |

| Example (Age 40, $500K coverage) | Term 20: ~$40-$50/month (non-smoker) | Whole Life: ~$400–$500/month (non-smoker) |

6. Why Whole Life Insurance Costs So Much More

You may have read somewhere about the idea of ‘buying term and investing the difference’ as a reason why people think that whole life insurance is a scam. If you purchased a term policy instead of whole life coverage you would save significantly on the amount of premium that you pay (at least in the early years of the policy). The difference in the premium from term insurance to whole life is pretty easily explained by the presence of the renewals in the term insurance policy. As you age your term insurance will become more expensive. Since whole life coverage has level premiums for the entire policy you pay more now, but much less later. A whole life policy prepays life insurance for you while you’re young to prevent it from getting very expensive later in your life. Whole life insurance premiums are made up of a few components:

- Embedded Savings/Investment Component: This is a ’forced-savings’ component of the plan, it grows tax-deferred inside the policy and is accessible to you in the future.

- Lifetime Guarantees: The policy will lay out guaranteed increases in cash value of the policy. This may be exceeded if the policy is eligible for dividends but this isn’t guaranteed. The increase in cash value of the base policy is guaranteed. As is the death benefit amount. Your beneficiaries are guaranteed to receive the death benefit because you cannot outlive a whole life insurance policy.

- Higher Early-Year Costs & Fees: By averaging the cost of insurance over your lifetime you pay higher rates right now for coverage than you need to in order to pay much less for the same insurance later in your life. There are also fixed costs from the insurer to run the policy. Things like administration, underwriting, policy servicing and commissions are all front loaded in the policy meaning that the setup and operating costs of the policy are mostly paid at the beginning.

7. The “Forced Savings” Argument: Pros and Cons

The main reason that you will find people thinking the whole life insurance is a scam is the ‘forced savings’ argument. Naysayers often feel like they were somehow misled on the value of the whole life insurance. There are pros and cons to the forced-savings side of whole life insurance:

Supporters Say — The Pros

- Built-in Discipline: You don’t get to skip the savings portion of the plan one month because you feel like it. Since it is included in the cost of keeping the plan active you will always contribute to it. The bottom line is that the key to a good savings plan is consistency, a mediocre plan that is consistently funded will often beat a perfect plan that isn’t.

- Guaranteed Growth: This is one of the few savings plan options that does offer guaranteed growth every year. While the returns may not be earth shattering in their amounts you know for sure that you will have more next year than you do this year.

- Long-Term Stability: Whole life insurance offers rewards to those who wait. Cash value growths accelerate later in the life of the policy so by maintaining the policy and focussing on it as a long term asset you will be rewarded.

- Behavioral Advantage: Forced savings provides you with an investment you don’t have to think about. There are no decisions you need to make, it happens automatically and avoids the opportunity to react emotionally to things like stock market ups and downs.

Critics Say — The Cons

Low Liquidity & Flexibility: You can’t easily pause or change your premium amounts. So if you face a sudden change in your personal cash flow this isn’t any area where you can alter the expense to reflect that.

High Opportunity Cost: Money in the cash value of a whole life insurance policy isn’t available to be invested elsewhere. This means that there is the chance that you can miss opportunities to invest in other areas like business expansion, stock markets or to pay down personal debts.

Slow Early Growth: While the long term rewards are strong you need to maintain focus on that. If you compare immediate returns between the cash values in a whole life insurance policy and alternative investments from outside a life insurance policy the short term returns will regularly favour the other investment.

Psychological Trap: Knowing that you must fund the premiums for your life insurance policy and that they include the forced savings portion can create some anxiety for people, particularly when they are facing income uncertainty.

| “Whole life isn’t a scam, it’s a disciplined insurance product that works best for people who never cancel.”

8. Cash Value: What It Is and What It Isn’t

The easiest comparison to make for people about what cash value is in a whole life insurance policy is that it is the policy’s built in savings account. Cash value builds inside the life insurance plan on a tax-deferred basis (there are Canadian rules regarding how fast it can grow and remain tax-deferred), the cash value belongs to the policy owner and is accessible while the life insured person is alive within certain guidelines. Cash value in a whole life insurance policy is not a bank account that you can freely draw money from at any time, it isn’t an investment that will perform like a mutual fund or other market-linked plan, and most of all it isn’t extra money that will be added to the death benefit of the policy when you pass away. In a very simplified version think of it this way. The portion of the premium that you pay that is allocated towards cash value is invested by the insurer to help fund the death benefit of the policy. The cash value is the fuel in the policy that helps power the plan to the guaranteed death benefit payout.

How Cash Value Actually Works

- Premium Allocation: Every premium is split internally within the policy. Some of it pays the insurance cost, some of it funds the expenses associated with operating the policy and some of it goes towards the plan’s cash value.

- Slow Growth: Since early on in a life insurance policy the set-up costs are higher, the plan needs to establish reserves and your insurance risk is being pre-funded the cash value grows more slowly initially because there is less premium left over after the other costs are addressed.

- Tax-Deferred Growth: As long as the policy passes something called ‘the exempt test’ the cash value within the plan grows each year without triggering taxable income for the policy owner. It is tax deferred and not tax free because if the owner accesses the cash value in the policy before the life insured person passes away there is the possibility that the withdrawal of cash will result in taxable income for the owner. Both cash loans and withdrawals can trigger taxable income.

- Loan Access: You are able to access the cash value in the policy in the form of a cash loan. This means that it is your plan to pay the money back into the policy and as such the death benefit remains unchanged. If there is a loan balance when the death benefit is paid the insurer retains the portion of the loan outstanding before paying the beneficiaries the remaining death benefit

- Withdrawal Option: There is also an option to withdraw cash value from the policy. This differs from a loan because it will often reduce the death benefit for the policy because you are removing cash without the intention of paying it back. A calculation will be made showing you how much the death benefit will be reduced for the amount of cash you are withdrawing from the policy.

- Insurer Investment: The insurer takes the cash value portion of the plan and invests it so that the growth can help fund the death benefit payout in the future.

- Early-Year Costs: There are higher administration costs for a life insurance policy in the early years of its existence. This includes many different factors related to the work involved in setting up the policy that aren’t in place forever, just during the early years of the policy.

The end result of this is that the cash value in your whole life insurance policy provides predictable, stable growth that is ideal for long term planning for things like your estate. It is not an investment tool that you should be looking at to help with any short term goals that you have.

Typical annual growth ≈ 2 – 4 % (net of fees).

Source: LIMRA Q2 2025 Canadian Life Insurance Sales Report and insurer dividend reports show average participating policy dividends around 4.5 %.

Accessing the Cash Value

- Borrow Against It: This is a loan where you receive some of the cash value of the policy but you tell the insurer that you intend to pay it back into the policy. There will be an interest rate charged on the loan internally so make sure that if you take out a loan you have a plan to repay it.

- Withdraw: This is also sometimes referred to as a ‘partial surrender’. You withdraw cash from the policy and the death benefit is reduced by the amount equivalent to the future value of what you are withdrawing today. What you will see is that if you withdraw $1000 from the policy it will reduce the death benefit by more than that amount so make sure you understand what you are giving up if you choose to make a withdrawal.

- Surrender: This is when you give up the coverage in its entirety. You receive all of the cash value from the plan and the contract terminates with no death benefit payable to beneficiaries in the future.

Tax Treatment in Canada

- Growth inside the policy: As long as the policy stays within the tax-exempt policy guidelines any growth within the policy is on a tax-deferred basis. Typically a whole life policy is designed at the outset to ensure that it remains exempt for its entire existence.

- Death Benefit: This is payable tax-free to named beneficiaries. There is no taxable income generated by the death benefit payment to beneficiaries.

- Withdrawals/surrenders: The policy has something called an ‘Adjusted Cost Basis (ACB)’ that is calculated to let you know how much of the cash value is accessible to you without triggering taxable income should you choose to borrow or withdraw funds from the cash value in the policy.

Source: Income Tax Act (Canada), Section 148 – Life Insurance Proceeds Exemption Published by the Department of Justice Canada

9. When Whole Life Insurance Works and for Whom

Just like with most financial products, whole life insurance isn’t for everyone. It is a single tool that can be very useful when it is deployed properly as a part of an overall financial security plan. Not everyone will have a need for whole life insurance and as mentioned earlier, it isn’t a tool to be used as part of any short-term savings strategy. When used as intended though, whole life insurance with cash value is a fantastic product that can be an important cog in your overall plan.

Who Benefits Most from Whole Life Insurance

- High-Income earners: High-income earners, often looked at as a benchmark of people earning in excess of $200k per year can benefit from the tax advantages that whole life insurance provides.

- Estate Planning: Since the death benefit is payable tax-free to beneficiaries, whole life insurance is a valuable tool to provide an infusion of needed cash that can help fund things like capital gains taxes owing on your estate.

- Tax-Efficient Wealth Transfer: Again since the death benefit payment is made tax-free to beneficiaries, whole life insurance is a very efficient way to pass wealth among generations. Outside of life insurance your investments will be deemed disposed of and your estate will need to pay taxes on the income triggered by that disposition. This can cause a really significant reduction to the value of your estate. Since life insurance death benefits aren’t taxable it is far more efficient to transfer wealth to future generations this way.

- Business Succession: Again the tax-free nature of the death benefit comes into play here. When you own shares in a business there are tax implications when you die. If you own a business the most cost effective way to handle the purchase of any outstanding shares when an owner dies is to have the funding in place via a whole life insurance policy.

- After Maxing RRSP & TFSA: If you have maxed out your RRSP and TFSA you are in a situation where finding places where your money can grow tax-deferred becomes challenging. The cash value in a whole life insurance policy is one of these tax-deferred places that you may be able to take advantage of.

Source: These use-cases align with CLHIA 2025 Facts Report (pp. 8–13) and LIMRA 2025 Canadian Life Insurance Sales Survey, which show permanent insurance ownership concentrated among high-income households.

10. Whole Life Insurance — Assessment

Is Whole Life Insurance Right For You?

Answer 4 quick questions to see if whole life insurance is right for you.

Why these questions?

These are based on industry-recognized suitability criteria from the

CLHIA 2025 Facts Report and LIMRA 2025 Canadian Life Insurance Survey,

showing that whole life insurance best fits high-income Canadians who’ve already maximized RRSPs and TFSAs

and are focused on estate planning or tax-efficient wealth transfer.

11. When Whole Life Doesn’t Work

Whole life insurance isn’t a great fit for every situation. It is important when you are looking at purchasing life insurance that you take the time to complete a needs analysis. This builds an understanding of how much life insurance you need and how long you need it for. Many large needs, like your mortgage, should not be covered by whole life coverage because the need doesn’t last your whole life. We suggest using term insurance for needs that go away (like mortgages or funding education for young children) and whole life coverage for things that are permanent (like funeral expenses or estate planning). Unfortunately part of the reason that whole life insurance is labelled as a scam is that it isn’t applied in the proper situations so someone who shouldn’t have had it in the first place feels like they were scammed into buying something that was more costly than they needed.

Who Should Avoid It

Here is a list of who should not buy whole life:

- Young families on a budget: This is a point in people’s lives when the needs tend to be at their highest. There may be a mortgage, there are costs associated with raising kids and there is income replacement to consider. All of these tend to be temporary needs though. Your mortgage will get paid off, kids grow up and mature families need less income replacement. Since these needs are large, trying to fund them with a whole life insurance policy would be expensive. Term insurance is often the better solution here.

- First-time insurance buyers: The first time you buy life insurance tends to be triggered by a financial event. We often see people looking for insurance for the first time after they get married, start a family or buy their first home. In these cases whole life coverage is probably not the best fit with its higher premiums and isn’t necessary because we are dealing with temporary needs, not permanent ones.

- Single parents needing income replacement: Again the cost/benefit needs to be reviewed. If you are a single parent you need to make sure that your kids are looked after in the event that you pass away. If the children are young this is a large need, but again it is temporary, so you can use term insurance for a more cost effective solution to your circumstance.

- Canadians still building emergency savings: Emergency savings are an important part of everyone’s financial plan. As we have mentioned, whole life insurance with cash value in it is not a good short term investment vehicle. Your emergency fund should be in an easy to access plan that provides stable growth regardless of the length of time it has existed. Using proper investment tools and not insurance policies is what you need to do for these types of savings.

- Those carrying high-interest debt (credit cards, lines of credit): You do need insurance to help your family pay off high interest debt, but term insurance is the choice here. Eventually the payments will go away, and the higher premiums for whole life coverage do not make sense when term insurance can be used to cover the need.

- People focused on retirement savings first: When you are focused on saving for retirement you can make use of the idea of buying term insurance for the protection you need with a lower premium and using the savings from that choice to invest more for your future. One word of advice though is don’t wait too long. If you build up a large RRSP you are adding to the potential tax burden on your estate. Whole life insurance can help make sure that there is money to pay that tax bill when it is needed.

- Short-term policyholders: Again this comes down to matching the need for coverage with the type of insurance you buy. If you only need coverage for short-term it doesn’t make sense to pay the extra for a whole life insurance plan.

- Individuals with fluctuating or uncertain income: Remember that the premium is not going to change with your whole life insurance plan. If you are unsure of your income in the future or have experience with large changes in your income it may not work to commit to paying the premium for whole life insurance right now.

- Anyone seeking investment growth over protection: This is simply something that can’t be repeated often enough when we are being asked to address if whole life insurance is a scam. It is not, it is a great insurance product that helps people plan for their future in many different ways. What it is not though is an investment plan. Often people who feel like they were scammed focused more on the idea that there is an investment component within the policy but that isn’t what whole life insurance is. If investment growth is your goal, use an investment product, not an insurance policy.

When It’s the Wrong Choice

Situations where whole life usually doesn’t make sense:

- Mortgage Protection: Your mortgage will decrease over the years and eventually be paid off. It is a temporary need and for temporary needs they are best covered with term insurance.

- Single-income households on a budget: Focussing on getting the amount of coverage you need for the most competitive premium may be your priority in this situation. If that’s the case don’t compromise coverage for a lower whole life premium. Use term insurance and get the amount of coverage you need.

- Young families just starting out: Again the expenses that you often encounter as a young family lean heavily towards the category of temporary ones. Children grow up, mortgages get paid off and income replacement needs fade over time. Fund large needs like these with term insurance to maximize the coverage you get for your premium dollars.

- Short-term financial responsibilities: Matching the time that you need the coverage to the length of the policy is essential in maximizing the effect of your premium dollars. If you use a whole life policy to cover a short term need you will pay more in premiums than you need to and given that the cash value in the policy grows more slowly in the early years of the plan you are unlikely to recoup the premiums you paid if you surrender the policy after the need goes away.

- First-time policyholders: Again, this is a circumstance where often the trigger for buying insurance (think, getting married, buying a home, etc.) is often something that you should be covering with a term insurance plan. This is the most straightforward, budget friendly solution available to you.

12. Case Study: Term Life + Investing the Difference

Below is a real-world example comparing a $500,000 whole life policy versus a 20-year term life policy + investing the premium difference in a TFSA or ETF portfolio.

| Sun Life Financial | Coverage | Annual Cost | Invested | 20-Year Outcome |

| Whole Life (Life Pay) | $500,000 | $4,920/year | — | ~$240,000 cash value after 20 years (2–4% annual growth) |

| Term 20 + Invest Diff. | $500,000 | $575/year | $4,345/year | ~$350,000–$385,000 TFSA/ETF value after 20 years (5–6% return) |

Rates sourced from LifeInsuranceCanada.com (Compulife data, Oct 29 2025).

What does this tell us? What you can see is that after 20 years the cash value in the whole life policy is less than the investment value from taking the difference between the premiums and putting them in an investment that grew at 5-6%. What this shows is that in the short term (typically up to 20 years) the buy term and invest the difference strategy will beat the cash value growth inside the whole life policy. If the case was extended though and you saw that typically at the renewal point a 20 year term plan has a premium that exceeds the premium for the whole life plan now you no longer have the ‘difference’ to invest and this is where the long term growth of the whole life policy cash value can start to close the gap that was created in the first twenty years.

13. The Tax Shelter Angle

Tax grind is a real concern for investors. If you invest outside of an RRSP or TFSA you typically will get a T slip that requires that you report any investment growth as income. This means that whatever I earn is reduced by the amount of tax owed. For example, if I invested $10,000 and earned 5% on it but was in a 30% marginal tax bracket the net effect is that I earn $500 in growth but I have to pay $150 in taxes. This means that I net $350 so my real rate of return is 3.5%, not 5%. One of the advantages of cash value growth inside a whole life insurance policy is that it is tax-sheltered growth. This means that the owner doesn’t pay taxes on the growth each year, taxable income is only triggered if the money is removed from the policy. Here are some terms that apply to whole life insurance and the tax sheltering of the growth within the policy.

| Concept | What It Means |

| Adjusted Cost Basis (ACB) | The difference between what you’ve paid into the policy and the portion used to actually pay for insurance. |

| Tax-Deferred Growth | Growth that is not taxed in the year it occurs, but is taxed in the year the money is taken out of the policy. |

| Policy Loans | A way to borrow money from the policy with the intent to pay it back so the death benefit doesn’t decrease |

| Collateral Loans | Using the cash value of the life insurance policy as collateral with a third party lender to secure a loan |

| Tax-Free Death Benefit | Proceeds of the policy paid out to named beneficiaries does not trigger taxable income for the beneficiary |

14. Why Some Advisors Push Whole Life Too Hard

Just like in all career paths it is an unfortunate truth that there will always be sales people who focus more on themselves and how a transaction affects them than whether or not it is the right choice for the client. The thought of the commission that they earn from the bigger premium that the whole life policy carries with it sometimes results in them making the recommendation to buy whole life insurance in circumstances where it isn’t the best solution. Remember, the agent that sells you a life insurance policy will make a commission no matter what type of insurance they sell you, and the percentage that they receive compared to the premium you pay doesn’t vary wildly from one product or company to another. The reason that they get paid more for whole life is that it carries the highest premium with it so the amount that the commission is based on is typically largest for whole life insurance policies.

The Incentive Problem

| Issue | Description |

| High Commissions | With the higher premiums associated with whole life come higher commissions as well. |

| Upfront Payouts | The commission for a sale is paid all up front to the advisor in a lump sum |

| Complex Illustrations | Sometimes the client doesn’t fully understand the complicated illustrations that show how a whole life plan works, making them rely fully on the recommendation of the advisor |

| Lack of Fee Based Advice | Fee based advice takes the commission right out of the equation. You pay a fee to the advisor to have them help you build a plan, no commissions are earned so the potential of suggesting a product because they would make more money is removed for the advisor. |

| Training Gaps | There are advisors who are newer to the industry and potentially a bit green that don’t fully understand all of the different solutions and where to apply different products. |

| Incentive Conflicts | Sometimes insurers will offer incentives to advisors that encourage the advisor to sell a specific product. This can result in someone making a recommendation based on achieving the incentive rather than the clients best interest |

| Consumer Impact | The consumer is impacted by the stories like we have discussed where people put out into the news that they’ve been scammed buying whole life insurance when the reality is that whole life insurance wasn’t the scam, it was more often than not the wrong product for their situation and now they feel scammed because they did overpay for the coverage that they needed or they feel like they were sold an underperforming investment. |

15. How to Spot Red Flags in a Sales Pitch

Given that there will be times when you may run across someone who is more focused on things like commission or other incentives than what is in your best interest we thought that it may be helpful to give you some red flags to listen for that may indicate that you need to seek out different advice before deciding to purchase anything.

- The policy pays for itself: This applies most commonly to participating whole life policies where they are eligible for dividends. The idea was that the dividends eventually grew large enough that they would cover the cost of the premium, but this is never guaranteed. If you feel like in the future you’ll have a hard time paying the premium you can’t rely on the policy ‘paying for itself’ so think twice about if this is the right solution for you.

- Guaranteed 7% returns: There are very few things in life that are guaranteed. The famous adage is that the only things are ‘death and taxes’. When it comes to annual rates of return you really need to ask hard questions if someone tells you that there is a guaranteed return unless you are talking specifically about GICs.

- Better than RRSPs or TFSAs: This is not true. RRSPs and TFSAs are investment plans that will behave differently than the values in your whole life insurance policy. If you want to make an investment use RRSP/TFSAs, not an insurance policy.

- You’ll never pay premiums again after x years: Again this is something that can’t be guaranteed so if you hear words like ‘never have to pay again’ you really need to question what someone is trying to sell you.

- Advisor avoids discussing surrender charges or early withdrawal penalties: You need to know if these exist so you don’t unexpectedly trigger fees and charges if you need to access the money.

- Pressure to sign today to lock in insurance rate: Insurance rates are based on your nearest age so unless today is exactly six months before your next birthday the cost of insurance is highly unlikely to change if you take a week or two to review things and maybe get a second opinion.

16. Expert Opinion

So is whole life insurance a scam? Instead of asking Reddit, let’s ask an expert who understands the product.

What Reputable Advisors and Experts Say

“Whole life isn’t a scam, what it is is a very powerful long term insurance product that can help you with estate planning, intergenerational wealth transfer and tax planning when used properly. It is not a replacement for an investment plan like an RRSP or TFSA. Your whole life insurance plan should be part of your overall financial security plan that should include both investment and insurance strategies to help you achieve your long term goals. — Simon Huften, President of LifeInsuranceCanada.com

17. How to Decide If Whole Life Is Right for You

Now that we understand that whole life insurance is not a scam we wanted to provide you with a guideline to help you figure out if it might be the right product for you. The following chart will help you with step-by-step questions to ask yourself with your answers leading you to the answer of ‘Is whole life insurance right for me?

Step-by-Step Decision Guide

| Step | Question | If “Yes” | If “No” |

| 1 | Have you maximized both your RRSP and TFSA? | Go to Step 2 | Start with term insurance first. |

| 2 | Is your annual income over $200,000? | Go to Step 3 | Term insurance and investing the rest makes more sense. |

| 3 | Looking to protect your estate and reduce your taxes? | Go to Step 4 | Term insurance works best for income protection. |

| 4 | Do you want life insurance that lasts a lifetime? | ✔️ Whole life insurance is a good fit. | ❌ Whole life insurance is not a good fit. |

Still unsure if whole life fits your needs?

If you tried to work through these questions and still feel unsure on if whole life insurance is the right fit for you then I suggest taking the time to reach out to LifeInsuranceCanada.com to speak to one of the expert advisors there who can help you figure out if whole life insurance is right for your unique circumstance. You can also use their website to compare quotes instantly if you are curious about premium rates.

Term Insurance Calculator

Compare Quotes Instantly

18. Alternatives to Consider Before Buying Whole Life Insurance

When considering life insurance you need to know that whole life insurance is not the only choice available to you. There are alternative products in the market place that can still provide you with the protection you need and may fit your situation better. Here’s a brief primer on each of these options:

- Term Life Insurance

Term life insurance provides you with coverage for a predetermined number of years at a set premium. There is no cash value in the policy so the cost tends to be lower because you are paying purely for the cost of the risk associated with the death benefit amount. One thing to remember is that since you are paying purely for the risk coverage, the older you are the higher the premium will be. This is important because term insurance has renewals built into it when the premium increases. For example, a ten year renewable term will have a premium increase every ten years and will typically expire when you are aged 80-85 (depending in the carrier).

Source: LIMRA 2025 Q2 Report – Term life policy growth +2 % year-over-year.

Consumer Reports. “Is Whole Life Insurance Right for You?” (Consumer Reports, 2015)

2. Universal Life Insurance

Universal life is similar to whole life in one key facet. That is that the premium is level for the entire contract and it doesn’t have an expiry date attached to it so it will cover you for your entire life. The difference from whole life comes from the way that the investment component of the policy works. Universal life has a minimum amount of premium you must pay every year to keep the policy in force but also a maximum amount you are able to deposit into the policy. For amounts in excess of the minimum required premium you are able to select from a list of investments (often similar to the insurers segregated funds) in which you can invest the money. These investment accounts can go up or down in value so you need to take care to make sure that the minimum requirements for the premium to keep the policy in force are maintained. Overall this can be a less expensive way to get coverage that lasts your entire life.

Source: CLHIA 2025 Facts Report, p. 12 – Universal life holds ≈ 15 % of individual coverage value in Canada.

3. Term Life + Self Directed Investing

If you are looking for an investment and insurance plan then the best idea may be to buy a term insurance policy instead of a whole life insurance policy. Take the difference between the term premium and the whole life premium and invest it in preferably a tax-deferred plan such as a TFSA. This allows you to both cover the needs if you pass away with the death benefit from the term insurance plan and maximize potential investment returns by utilizing proper investment products. The key to this strategy is discipline, far too often the ‘buy term and invest the difference’ switches to ‘buy term and spend the difference’ every month and that doesn’t help achieve your long-term goals.

19. FAQ

No. It is an insurance plan that plays a valuable roll in overall financial plans when applied properly.

Too often people who feel like whole life insurance is a ripoff were sold the wrong product for their situation or were sold on whole life insurance as an investment plan. It is not an investment plan and should not be used as one.

Estate planning, tax planning and intergenerational wealth transfer are a few areas where whole life insurance is an ideal solution for someone who wants to include these aspects in their financial plan.

Whole life coverage will have a higher premium initially than term insurance does but whole life premiums never change and term life premiums renew so eventually (often after about 20 years of policy life) the term policy will become more expensive. When compared to universal life premiums whole life premiums will be higher than the minimum funding required for the universal life policy. The big reason for this is that a minimum funded universal life insurance plan will have no cash value in it. Whole life has the forced savings component that universal life doesn’t which results in whole life insurance having a cash value.

Whole life insurance is different from your TFSA and RRSP and shouldn’t be confused with either. For investment purposes you should focus on using your TFSA and RRSP before you consider using a whole life insurance policy as an investment.

20. Key Takeaway

Hopefully by now you see that while it is sometimes misunderstood, whole life insurance is not a scam. It is a powerful financial planning tool that is extremely useful when applied properly. If someone suggests to you that you use it as a short term investment product that is simply bad advice and you should question not only the advice but what is motivating the person who gives you that advice. If it is suggested to you for use as an estate planning or high level tax planning solution that is often a more appropriate situation where you would use whole life insurance.

For many people what they will see is that the majority of their major insurance needs are temporary in nature. We’ve mentioned the big ones in this article already but it bears repeating here. Insurance needs for things like your mortgage, income replacement or supporting dependent children are typically far better suited to be taken care of using term insurance which can get you the same death benefit as whole life insurance but often for a significantly lower premium.

When you are deciding if whole life insurance is the right plan for you make sure that you assess your needs properly. If you need help, seek out the advice from an expert like the team at LifeInsuranceCanada.com where they can help you decide what is the best solution for your overall financial plan. Remember, whole life insurance policies should not be something that you purchase to take the place of your TFSA or RRSP. Use insurance to manage risk and use investment plans to grow your savings.

21. Conclusion & Final Verdict

Whole life insurance isn’t a scam. Unfortunately it is a product that is sold in situations where it isn’t the best solution and that makes people feel like they were sold something that they didn’t understand and didn’t need. The best plan of attack for many people is to build a financial plan that includes risk management strategies using life insurance as part of that plan. This will often begin with you setting up a term insurance plan to provide immediate financial support if you pass away unexpectedly. As you grow with your plan you may need to revisit the idea of whole life coverage based on needing to improvise your overall estate and tax efficiency plans but that isn’t where most people will start. Visit LifeInsuranceCanada.com to get personalized quotes for all of your life insurance needs. This will allow you to see how every part of your financial plan can fit together.

About the Author

Simon Huften, President of LifeInsuranceCanada.com a licensed life insurance advisor with over 15 years of experience helping Canadians choose the right coverage.

Compare whole life vs term life quotes now

Get a free quote

Request a whole life and term insurance quote

Disclaimer: The information provided in this article is for general educational purposes only and does not constitute personal financial or insurance advice. Always consult a licensed insurance advisor before making financial decisions.