Term Life Insurance

Term Life Insurance Permanent Life Insurance

Permanent Life Insurance No Medical Life Insurance Canada

No Medical Life Insurance Canada Critical Illness Insurance

Critical Illness Insurance

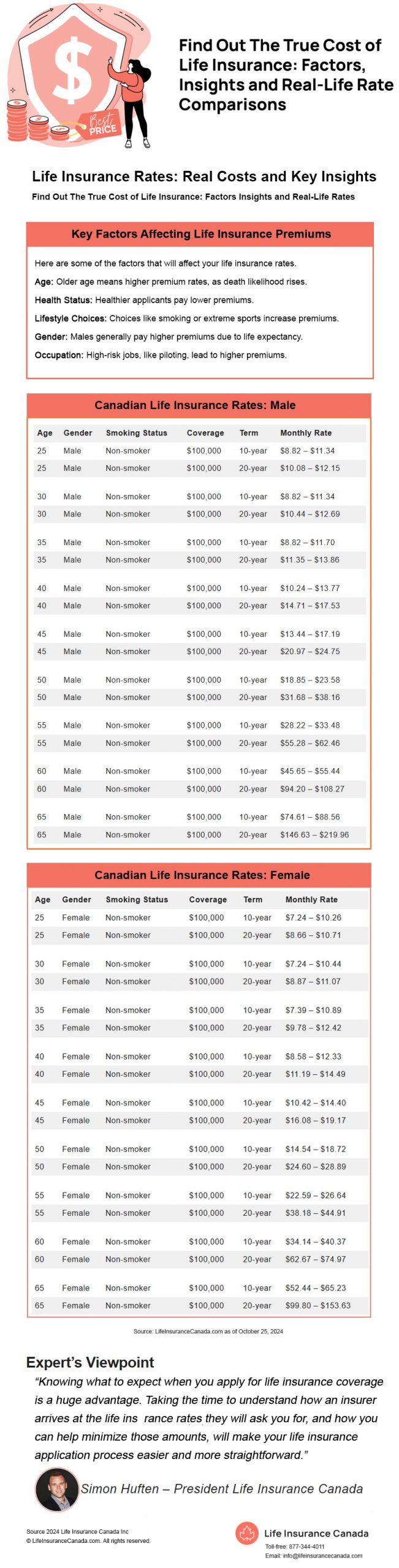

Find Out The True Cost of Life Insurance: Factors, Insights and Real-Life Rate Comparisons

One of the most common things that we hear as a reason why someone chooses not to get life insurance, even when they understand the need for it, is that they think that it will cost too much. The perception is that life insurance rates are a complicated issue and will definitely be expensive, this isn’t true and you should understand that what you pay for life insurance depends on a number of factors. In this article we are going to explore what you need to know about life insurance rates so you can make an informed decision on getting coverage. Understanding how life insurance rates are determined can also help you with any current coverage you have if you are looking at ways to optimize your coverage. Read on to find out the different things that will affect your life insurance rates and get some tips on how to get the best rates as well as a quick snapshot of what average life insurance costs are in Canada.

Overview

Here’s a quick overview overview of what we will cover in this article:

- How are life insurance rates calculated? This will give you an idea of what an insurer looks for when they are calculating your life insurance rate.

- Factors that influence life insurance rates. This will highlight some of the main areas that influence how much your insurance premium will be.

- The different types of life insurance and how what type of insurance you apply for will play a role in the rate calculations. Different styles of insurance will calculate rates differently so understanding what you are applying for is important as well.

- Some tips and strategies for reducing your life insurance rates. Some of the things that influence the calculations of your life insurance rates are within your control. We will give you some ideas as to how you can help limit the things that increase your life insurance rates.

- An introduction to the top insurers in Canada and how they compare to one another.

How Are Life Insurance Rates Calculated?

Life insurance rates in Canada are calculated based on a series of factors. At the core of what your life insurance rates are is the idea that a life insurance company reviews your application and weighs the risk factors that you bring to the table. The higher the risk, the more you will pay. An analogy that may help you see this is comparing it to a different style of insurance. If you live in a neighbourhood with an excessively high rate of auto theft you pay more for car insurance because the risk that the insurer will pay out your policy because of theft is higher. The same is true for life insurance. Some of the factors that affect your life insurance rates are within your control and some are not, but they all affect your life expectancy and as a result play a role in the premium that you pay for your policy. Let’s take a look at the factors that influence the life insurance rates you pay as a policy owner.

Factors That Influence Life Insurance Rates

Life insurance companies are in the business of risk management, and they want to make sure that the rates that they charge result in a fair premium for each policy owner. A 28 year old non-smoking person who runs 3 marathons a year should not pay the same for life insurance as a 60 year old who leads a sedentary life and smokes a pack a day. The risk is different and the life insurance rate that they each pay should reflect that. Here are some of the factors that will affect your life insurance rates.

…insurers use family history, lifestyle and medical information to set prices that fairly reflect the level of risk of insurance applicants.“

— Stephen Frank, President and CEO of the Canadian Life and Health Insurance Association (CLHIA) Source

Personal Factors

- Age – Simply put, the older you are, the higher the premium rate you will pay. I say this a bit tongue in cheek, the last time we checked, everyone dies. One thing I know for sure is that as you age you are getting closer to the end of your life. I also know that the odds that you are going to die each year get higher, and not in a linear way. Every year that you age the odds that it will be your last birthday are higher than they were the previous year. Sorry to be the bearer of bad news, but this is a reality. So the older you are when you apply for life insurance, the higher the premium will be for that policy.

- Health Status – How healthy you are at the time that you apply for coverage plays a role in the rate that you will pay. Again, this is based on the risk factors to the insurance company. Someone in good health is a much better risk than someone who has health issues. As a result, people who are healthy at the time of application pay lower insurance rates.

- Lifestyle Choices – This is a category where you can definitely influence your life insurance rates. Choices like becoming a smoker, consuming excessive amounts of alcohol, having a poor driving record or participating in extreme sports all add to the risk associated with offering you life insurance. As a result, if you choose to make these activities part of your life you can expect to pay higher life insurance premiums.

- Gender – If you look at life expectancies, males and females are expected to live for different lengths of time. In Canada the male life expectancy is 79.8 years and for females it is 83.9 years. Since males tend to have shorter lives than females a life insurance company faces the reality that they will likely pay the death benefit on a male earlier than that of a female. Since they expect to collect the premiums longer for a female the rates that they pay are lower than for males.

- Occupation – Certain jobs carry higher risks with them than others. When you are an insurance company and you have to calculate life insurance rates based on the odds that you will die this plays a role in the decision. For example, being a pilot carries a higher risk as an occupation. This means that pilots pay more for life insurance than someone who works as an accountant (as an example). There are inherent risks with some jobs that need to be factored into the calculation of the premium for the policy.

Policy Related Factors

Aside from the personal factors that influence life insurance rates it is also true that the type and amount of life insurance that you apply for will affect the rates as well. Some of these factors are:

- Type of Policy – Depending on if you apply for term insurance, whole life, participating, or universal life insurance you will see a different premium calculation. This is because of various factors. For example, term insurance will be the least expensive initially because these policies have renewals built in where the premium increases at set times in the future, so as the risk that you die increases the insurer has built in protection because the premium is set to increase to offset that risk accordingly. The other permanent styles of insurance charge a fixed premium for the duration of the policy so you will pay more as a younger person but that rate is locked in for your life.

- Coverage Amount – How much coverage you apply for affects your life insurance rates as well. Sometimes not in the way that you would think though. Every company has different guidelines for underwriting, but typically as death benefit amounts increase, so does the amount of information the insurer wants to collect about you. This means that the insurance company can make a more informed decision and can offer better rates as the amount of the policy increases. As an example, if you are applying for an amount of coverage where the decision is based purely on a questionnaire you answer compared with an amount where the insurer requires a questionnaire as well as blood tests, urinalysis and a report from your doctor, the more information allows them to make a more informed decision and as such they can offer better rates (per dollar of death benefit) with this information available to them.

- Policy Duration – When you choose to take a term life insurance policy the duration of each term influences the rate you pay as well. This is because the duration is how often the insurer can increase the premium, which helps them offset the risk as you get older. If you choose a ten year duration the initial premium will be lower than if you choose a twenty or twenty five year duration. This is because for the ten year plan there are renewals that will increase the rate during the time that the longer policies have the premium locked in.

- Additional Riders – You are able to add features to your life insurance plan that will affect the rates you pay. If you add a rider where the premium is paid should you become disabled, or add on a benefit that pays if you are diagnosed with a critical illness you will see the rate that the policy has associated with it goes up as well. This is because these riders increase the risk to the insurer and as a result they will charge a higher premium to offset that risk

Types of Life Insurance Rates

One major factor in the way that your life insurance rates will be calculated depends on what type of life insurance policy you pay for. There are differences in the way that term insurance and permanent insurance rates are determined.

- Term Life Insurance Rates – Term life insurance rates are a very ‘pure’ form of insurance. Term life has no cash values included in it and there are renewal points in the plan that lay out how the premium will increase as time passes. As a result what you often see is that for a similar death benefit amount term life insurance rates initially will be less than the rates for the same death benefit in permanent coverage. As time passes this will reverse due to the renewal increases included in the policy.

- Permanent Life Insurance Rates – Whole Life Insurance Rates are set at the time of application and will not change for the entire premium paying period of the policy. These policies include a cash value component which reflects the fact that early on in the life of the policy, the premium that you pay is more than the actual cost of the insurance that the plan provides. Think of whole life insurance in this way. In a very simplified way, you are paying a higher premium for the life insurance early on in the contract so that later on in your life you pay a lot less. Overfunding it early allows this to happen.

- Universal Life Insurance Rates – Universal life insurance differs from whole life in one key way. That way is the presence of an investment account inside the policy that you control. You make ‘deposits’ into your universal life account and on a monthly basis the insurer comes and removes the premium from that account. You are able to deposit (within limits) amounts higher than the monthly premium and the universal life account can grow (or decrease) in value based on the performance of the investments you choose within the plan. Typically today you will see a level cost selected for the insurance premium, meaning that the life insurance rates are set at the time of application and will not increase as you age.

Tips for Lowering Life Insurance Rates

It is possible to make changes to the controllable parts of your life insurance application that can improve the rates that you are offered.

- Improving Health and Lifestyle – making choices to improve your health by taking steps to stop smoking, lose weight or give up your skydiving hobby will provide you with the opportunity to have improved rates available to you.

- Choosing the Right Coverage Amount – completing a needs analysis to make sure that you aren’t applying for significantly more coverage than you may need is a good way to keep your life insurance rates in check.

- Considering Term Length – Since term insurance provides you with the most cost effective way of getting life insurance try and match the time that you need the coverage with the length of term policy that you choose. For example, if your mortgage is set to be paid off in 19 years you may want to choose a 20 year term plan. This eliminates the renewals where the premium increases during the time that you need the coverage, allowing for budget certainty regarding the amount you will pay in premiums.

- Bundling with Other Insurance Policies – Included in the life insurance rates that apply to a policy are fixed administrative costs associated with each policy. Some insurers may allow you to ‘bundle’ many policies together making it so that you only pay one set of administration fees rather than paying the fees for each individual policy.

Strategies To Get The Best Life Insurance Rates

Here are a few strategies you can employ in areas that most commonly affect life insurance rates for new applicants.

- Improving health and lifestyle factors – making different choices can reduce your rates. For example, if you quit smoking and you successfully go without using any nicotine products for a period of 12 months you can be classified as a non-smoker and save significant amounts of premium.

- Timing your purchase strategically – did you know that many insurance policies are issued on an ‘age-nearest’ basis. This means that you have six months after your birthday where you count as your current age, after that you are closest to the next age and will pay a higher rate.

- Leveraging group rates and employer-sponsored options – if you have a hard time qualifying personally for insurance but your employer offers benefits you may want to explore additional coverage via your work plan. Many benefit plans have something called a ‘non-evidence maximum’ associated with them that is an amount of death benefit you can have with no medical questions. Take advantage of this if you are having a hard time with personally issued policies.

- Comparing multiple policy quotes – not all insurers treat things equally. You may find that one company is more forgiving with their life insurance rates than another based on a variety of circumstances. Comparing quotes from different companies will help you find the best one for your individual circumstance.

- Opting for term life insurance over whole life – with its built in renewals term life insurance is able to offer you a larger death benefit today than whole life coverage will for similar premium dollars. Just make sure that you aren’t trying to cover a permanent need with temporary solution.

- Paying premiums annually instead of monthly – In most cases (universal life is the main exception) you receive a better rate if you pay your premium once annually instead of every month. This comes down to a number of reasons but a big one is administration costs, the insurer is processing one payment instead of twelve, so less work for them means lower rates for you

- Avoiding unnecessary add-ons or riders – adding riders to your policy that pay off if you die as the result of an accident or other extra features may seem like a nice way to boost your coverage, but don’t do this at the expense of the actual death benefit of the policy. If you can only afford a fixed amount of premium make sure that the death benefit satisfies your needs analysis before adding bells and whistles to your policy.

- Working with an independent broker for unbiased advice – this may be the best advice in general. An independent insurance broker will help you find the best life insurance rates for you based on their comprehensive knowledge of the industry. It is their job to help you get the best bang for your buck on premium dollars.

How to Compare Life Insurance Rates From Different Insurers

One of the best ways to compare life insurance premiums is to make use of an online calculator. Depending on what website you are using you can often get instant quotes from many different insurers to make it easier to compare identical amounts of coverage and see what the life insurance rates are for the death benefit you would like to have.

At LifeInsuranceCanada.com we provide instant quotes in 2 separate categories.

- We have a term insurance calculator that can provide you with instant quotes based on the amount of death benefit and term length you select.

- There is a calculator that will show you rates for permanent insurance products. Again, you enter in the calculator if you would like to see rates for whole life or universal life plans and you will receive rates from a number of carriers for you to compare.

Another way that lifeinsurancecanada.com provides online support is that if you aren’t sure how much death benefit to enter into the calculation take advantage of the ‘Calculate Coverage’ button that will walk you through a needs analysis that helps you figure out how much insurance your beneficiaries need you to apply for.

What Will Life Insurance Cost Me?

Top 10 Life Insurance Rate Providers In Canada

Here’s a ranked list of the top 10 life insurance companies in Canada based on market reputation, financial stability and product offerings:

- Manulife

- Sun Life Financial

- Canada Life

- RBC Insurance

- Desjardins Insurance

- BMO Insurance

- Empire Life

- iA Financial Group

- Equitable

- Canada Protection Plan

Manulife

Manulife Financial Corporation is a leading international financial services provider that helps people make their decisions easier and lives better. With our global headquarters in Toronto, Canada, we provide financial advice and insurance, operating as Manulife across Canada.

Manulife. (n.d.). About Us. Retrieved from Manulife

Example: Manulife Life Insurance Rate Illustration: A 40 year-old non-smoker might pay $14.90 per month or $166.44 per year for a 20-year term with $100,000 Family-Term™ policy.

Sun Life Financial

Sun Life is one of the largest public companies in Canada. Our financial strength ratings are some of the highest in the industry. You can find shares of Sun Life Financial Inc. (SLF) are listed on the Toronto (TSX), New York (NYSE) and Philippine (PSE) stock exchanges.

Our businesses are widely varied. We strike a balance between protection and wealth businesses. We operate in countries in many parts of the world. And our Clients include individuals, groups and institutions. We manage risk so we can steer through uncertain and volatile markets. That lets us help our Clients, no matter what the markets are doing.

Sun Life. (n.d.). Who We Are. Retrieved from Sun Life

Example: Sun Life Insurance Rate Illustration: A 40-year-old non-smoker might pay $18.36 per month for a Sun Life Evolve™ 20-year term policy with $100,000 coverage.

Canada Life

For more than 175 years, our customers across Canada have trusted us to provide for their financial security needs and to deliver on the promises we have made.

Today, Canada Life provides insurance, wealth management, and healthcare benefit products and services in Canada, the United Kingdom, Isle of Man and Germany, and in Ireland through Irish Life.

Canada Life. (n.d.). About Us. Retrieved from Canada Life

Example: Canada Life Insurance Rate Illustration: A 40-year-old non-smoker male might pay $17.53 per month or $194.81 per year for a 20-year term life with $100,000 My Term™ policy.

RBC Insurance

RBC Insurance® offers a wide range of life, health, home, auto, travel, wealth and reinsurance advice and solutions, as well as creditor and business insurance services to individual, business and group clients.

RBC Insurance is the brand name for the insurance operating entities of Royal Bank of Canada, Canada’s biggest bank, and one of the largest in the world based on market capitalization.

RBC Insurance. (n.d.). About Us. Retrieved from RBC Insurance

Example: RBC Life Insurance Rates Illustration: A 40-year-old non-smoker male might pay $17.55 per month or $195.00 per year for a 20-year term with $100,000 YourTerm™ policy.

Desjardins Insurance

The largest financial cooperative in North America

It’s all about people 7.7 million members and clients 56,165 employees 2,379 elected directors

Ranked by Mediacorp Canada Inc. among Canada’s Top 100 Employers, Top Employers for Young People, and Greenest Employers Received Women in Governance’s Platinum Parity Certification, which recognizes the steps we’re taking toward achieving equal representation of women at every level of the organization

Desjardins. (n.d.). Quick Facts: Who We Are. Retrieved from Desjardins

Example: Desjardins Life Insurance Rates Illustration: A 40-year-old non-smoker male pays $34.56 per month or $384.00 per year for a Life Term 20™ policy with $100,000 coverage.

BMO Insurance

BMO Insurance provides a wide range of life insurance products, including term and permanent life policies. Their offerings are integrated with their broader financial services, making them a trusted name.

BMO Insurance is founded on a legacy that extends back to 1817. This proven history of financial strength lets us stand behind our insurance products by offering flexible coverage options, comprehensive benefits and competitive prices. A.M. Best Company gives us a Financial Strength Insurer Rating of A1, recognizing our excellent ability to meet our obligations.

BMO Insurance. (n.d.). About Us. Retrieved from BMO Insurance

Example: BMO Life Insurance Rates Illustration: For a 40-year-old non-smoker male with a 20-year term policy, coverage of $100,000 costs $18.72 per month or $208.00 per year.

Empire Life

Empire Life is one of the top 10 Canadian life insurance companies. Empire Life’s mission is to make it simple, fast and easy for you to get the investment, insurance and group benefits coverage you need to build wealth, generate income, and achieve financial security. Based in Kingston, Ontario and with offices from coast to coast.

Empire Life. (n.d.). About Us. Retrieved from Empire Life

Example: Empire Life Insurane Rates Illustration: A 40-year-old non-smoker male pay $15.93 per month or $177.00 per year for a 20-year term life policy with $100,000 Solution 20™ policy.

iA Financial Group

iA Financial Group is one of the largest insurance and wealth management groups in Canada, with operations in the United States. Founded in 1892 iA offers 5 types of life insurance to meet your needs:

- Term life insurance: affordable coverage to meet your temporary needs. 2. Permanent life insurance: lifetime insurance coverage permanently protects your family and your legacy. 3. Participating life insurance: permanent life insurance that ensures the growth of your estate. 4. Universal life insurance: a combination of permanent life insurance and savings. 5. Specialized life insurance: specialized life insurance to build and protect your wealth.

iA Financial Group. (n.d.). About Us. Retrieved from iA Financial Group

Example: Industrial Alliance (iA) Life Insurance Rates Illustration: A 40-year-old non-smoker pays $16.38 per month or $182.00 per year for a $100,000 Pick-A-Term™ policy.

Equitable Life of Canada

Equitable offers a diversified lineup of competitive products which can help you achieve your financial goals with confidence. Equitable has a broad range of insurance products to meet all your life and health insurance needs. Find out which life insurance solution is right for you!

Term life insurance offers affordable protection with a choice of premium payment options to fit your budget.

Equimax participating whole life insurance policies that offer guaranteed premiums, cash values and death benefit. The cash value can be accessed to fund education, renovate your home or even supplement your retirement income.

Equitable Life. (n.d.). Individual Insurance. Retrieved from Equitable Life

Example: Equitable Life Insurance Rates Illustration: A 40-year-old non-smoker male pays $15.78 per month or $181.95 per year for a 20-year term policy with $100,000 coverage.

Canada Protection Plan

Canada Protection Plan is a Canadian owned and operated corporation that designs, markets and provides life insurance and related products with simplified underwriting processes that require no medical exams on most of our plans. Canada Protection Plan products can be purchased through over 25,000 independent insurance advisors across Canada or through our own Licensed Insurance Advisors by contacting our Call Centre.

Canada Protection Plan. (n.d.). About Us. Retrieved from Canada Protection Plan

Example: Canada Protection Plan Life Insurance Rates Illustration: A 40-year-old smoker could expect to pay $17.01 per month or $189.00 per year Express Elite™ 20 Year Term with $100,000 coverage.

Canadian Life Insurance Rates

Table: Male Term Life Insurance Rates

INSIGHTS

The monthly term insurance rates for both the 10-year and 20-year term insurance policies increase with age. The charts show that younger people benefit from much lower rates, while older people see a sharper increase, especially when it comes to longer coverage terms.

| Age | Gender | Smoking Status | Coverage | Term | Monthly Rate |

| 25 | Male | Non-smoker | $100,000 | 10-year | $8.82 – $11.34 |

| 25 | Male | Non-smoker | $100,000 | 20-year | $10.08 – $12.15 |

30 | Male | Non-smoker | $100,000 | 10-year | $8.82 – $11.34 |

| 30 | Male | Non-smoker | $100,000 | 20-year | $10.44 – $12.69 |

35 | Male | Non-smoker | $100,000 | 10-year | $8.82 – $11.70 |

| 35 | Male | Non-smoker | $100,000 | 20-year | $11.35 – $13.86 |

40 | Male | Non-smoker | $100,000 | 10-year | $10.24 – $13.77 |

| 40 | Male | Non-smoker | $100,000 | 20-year | $14.71 – $17.53 |

45 | Male | Non-smoker | $100,000 | 10-year | $13.44 – $17.19 |

| 45 | Male | Non-smoker | $100,000 | 20-year | $20.97 – $24.75 |

50 | Male | Non-smoker | $100,000 | 10-year | $18.85 – $23.58 |

| 50 | Male | Non-smoker | $100,000 | 20-year | $31.68 – $38.16 |

55 | Male | Non-smoker | $100,000 | 10-year | $28.22 – $33.48 |

| 55 | Male | Non-smoker | $100,000 | 20-year | $55.28 – $62.46 |

60 | Male | Non-smoker | $100,000 | 10-year | $45.65 – $55.44 |

| 60 | Male | Non-smoker | $100,000 | 20-year | $94.20 – $108.27 |

65 | Male | Non-smoker | $100,000 | 10-year | $74.61 – $88.56 |

| 65 | Male | Non-smoker | $100,000 | 20-year | $146.63 – $219.96 |

Canadian Life Insurance Rates

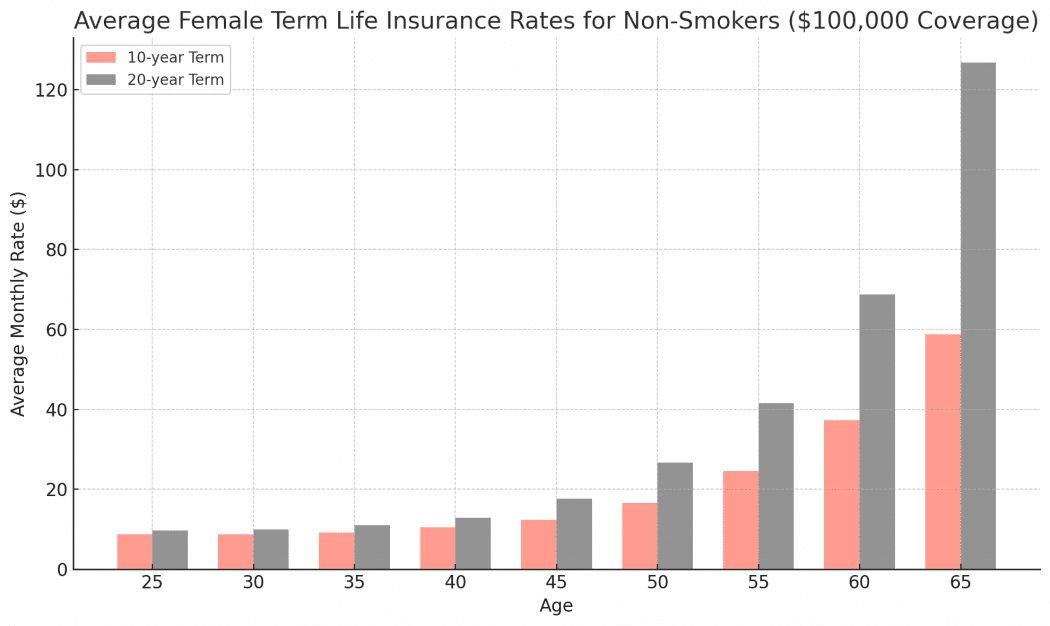

Table: Female Term Life Insurance Rates

INSIGHTS

Similar to the male term insurance rates, the monthly rates for both the 10-year and 20-year term policies increase with age.

Females in general have lower insurance rates compared to males at every age level and the same increase in rates for olderpeople is observed. In summary, younger people pay significantly less for life insurance and females benefit from slightly lower rates compared to males. The cost difference between 10-year and 20-year term policies becomes more noticeable as age increases.

| Age | Gender | Smoking Status | Coverage | Term | Monthly Rate |

| 25 | Female | Non-smoker | $100,000 | 10-year | $7.24 – $10.26 |

| 25 | Female | Non-smoker | $100,000 | 20-year | $8.66 – $10.71 |

30 | Female | Non-smoker | $100,000 | 10-year | $7.24 – $10.44 |

| 30 | Female | Non-smoker | $100,000 | 20-year | $8.87 – $11.07 |

35 | Female | Non-smoker | $100,000 | 10-year | $7.39 – $10.89 |

| 35 | Female | Non-smoker | $100,000 | 20-year | $9.78 – $12.42 |

40 | Female | Non-smoker | $100,000 | 10-year | $8.58 – $12.33 |

| 40 | Female | Non-smoker | $100,000 | 20-year | $11.19 – $14.49 |

45 | Female | Non-smoker | $100,000 | 10-year | $10.42 – $14.40 |

| 45 | Female | Non-smoker | $100,000 | 20-year | $16.08 – $19.17 |

50 | Female | Non-smoker | $100,000 | 10-year | $14.54 – $18.72 |

| 50 | Female | Non-smoker | $100,000 | 20-year | $24.60 – $28.89 |

55 | Female | Non-smoker | $100,000 | 10-year | $22.59 – $26.64 |

| 55 | Female | Non-smoker | $100,000 | 20-year | $38.18 – $44.91 |

60 | Female | Non-smoker | $100,000 | 10-year | $34.14 – $40.37 |

| 60 | Female | Non-smoker | $100,000 | 20-year | $62.67 – $74.97 |

65 | Female | Non-smoker | $100,000 | 10-year | $52.44 – $65.23 |

| 65 | Female | Non-smoker | $100,000 | 20-year | $99.80 – $153.63 |

Infographic: Life Insurance Rates Real Costs and Key Insights

Expert’s Viewpoint

“Knowing what to expect when you apply for life insurance coverage is a huge advantage. Taking the time to understand how an insurer arrives at the life insurance rates they will ask you for, and how you can help minimize those amounts, will make your life insurance application process easier and more straightforward.”

Simon Huften – President Life Insurance Canada

Life Insurance Rates for Smokers and Non-Smokers

How Do Smoking Habits Affect Life Insurance Rates?

The health risks that are associated with the use of nicotine products have been proven oevr and over. Nicotine users face higher risks of lung disease, heart disease and cancer. Knowing this information, when an insurance company is calculating the life insurance rates for a smoker they will be higher than a non-smoker. In a paper published using research from the University of Toronto, they observed that smokers between the ages of 40 and 79 had a risk of dying that was almost three times higher than non-smokers in the same age group. This information is why the life insurance rates are higher for smokers. Simply put, smoking reduces your life expectancy.

If you are a non-smoker you can potentially benefit in other ways as well. Some insurers will off rates that are preferred or super-preferred to non-smokers. This means that a non-smoker that is in excellent health your life insurance rate may be lower than the originally quoted premiums because you are doing so well maintaining a healthy lifestyle.

Definition of a Smoker in Life Insurance Terms

What does it mean to be a smoker in the eyes of an insurance company? Most insurance companies classify you as a smoker if you have used any tobacco or nicotine products within the last 12 months. This includes cigarettes, cigars, pipes, chewing tobacco, and nicotine replacement products like patches and gum. This will also include vape users. Although nicotine has a short lifetime in your bloodstream, there are by-products of nicotine use that remain in your system for long times. It is these markers that an insurance company will test for when they order blood work to be carried out during your application. Even if you are someone who considers themselves an ‘occasional smoker’ you will often be classified as a smoker. There is little gray area in the eyes of the insurers when it comes to smoking and the use of tobacco products.

How Long After Quitting Will Rates Improve?

In that same University of Toronto story mentioned earlier, they point out how there are health advantages available to anyone who currently smokes. Quitting smoking can restore some of the life expectancy that was lost during the years you smoked. If you do make the choice to quit smoking you could be eligible to have a policy change processed where you could have your life insurance rates recalculated based on you now being a non-smoker. Typically an insurer will insist on a period of 12 consecutive months where no nicotine products have been used. It also needs to be a choice you made, not something that your doctor told you that you needed to do because you just had a heart attack.

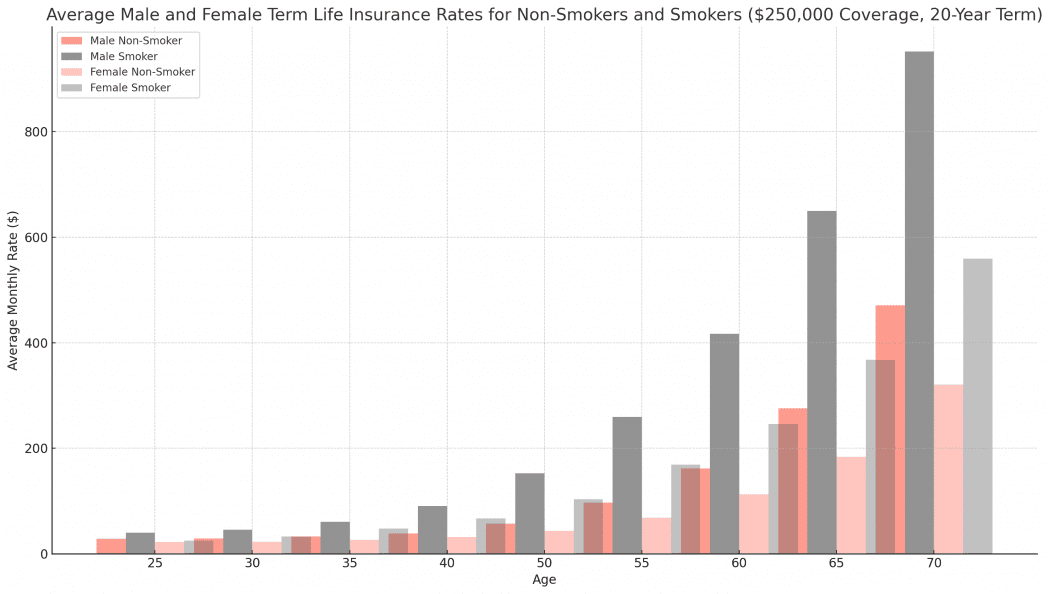

Smoker vs. Non-Smoker Life Insurance Rates

Here is a table that provides a detailed comparison of life insurance rates for smokers and non-smokers, broken down by age group, gender and term length.

INSIGHTS

As you age, life insurance rates increase drastically, especially after age 50. Smokers usually pay higher premiums than non-smokers and as they get older the cost gap widens. Generally, males have higher term insurance rates than females across all age groups.

| Age | Gender | Term | Coverage Amount | Non-Smoker Monthly Rate | Smoker Monthly Rate |

| 25 | Male | 20 | $250,000 | $15.98 – $41.63 | $29.03 – $51.53 |

| 25 | Female | 20 | $250,000 | $11.93 – $32.85 | $18.00 – $31.67 |

| 30 | Male | 20 | $250,000 | $15.98 – $42.75 | $31.73 – $59.63 |

| 30 | Female | 20 | $250,000 | $12.60 – $32.85 | $22.75 – $42.53 |

| 35 | Male | 20 | $250,000 | $18.74 – $46.58 | $43.88 – $77.40 |

| 35 | Female | 20 | $250,000 | $14.66 – $38.03 | $34.14 – $60.98 |

| 40 | Male | 20 | $250,000 | $26.26 – $51.08 | $70.65 – $110.70 |

| 40 | Female | 20 | $250,000 | $19.75 – $43.43 | $49.75 – $83.70 |

| 50 | Male | 20 | $250,000 | $40.65 – $73.13 | $113.62 – $191.93 |

| 50 | Female | 20 | $250,000 | $29.27 – $58.28 | $71.88 – $135.00 |

| 55 | Male | 20 | $250,000 | $67.08 – $126.68 | $179.35 – $339.75 |

| 55 | Female | 20 | $250,000 | $46.03 – $90.68 | $109.68 – $228.83 |

| 60 | Male | 20 | $250,000 | $120.60 – $203.40 | $289.56 – $544.28 |

| 60 | Female | 20 | $250,000 | $82.47 – $142.43 | $172.19 – $319.50 |

| 65 | Male | 20 | $250,000 | $216.00 – $335.70 | $450.03 – $849.83 |

| 65 | Female | 20 | $250,000 | $145.31 – $222.08 | $257.55 – $478.35 |

| 70 | Male | 20 | $250,000 | $357.58 – $584.55 | $676.59 – $1226.25 |

| 70 | Female | 20 | $250,000 | $240.51 – $400.28 | $418.81 – $699.53 |

Comparing Premiums Across All Insurance Products

There are different styles of life insurance and they all have different rates associated with them Each different type will suit a different need quite well.

Term Life Insurance: Term life insurance offers a set amount of coverage for a specific premium for a fixed amount of time (the ‘term’ of the policy). Typically you will see 10 or 20 years as the length of the term. When the policy gets to the end of a term there will be a renewal where the premiums increase. Term insurance is ideally suited for covering your needs for large, temporary expenses (like a mortgage) because it is the most affordable way of offsetting this type of need.

Whole Life Insurance: Whole life insurance offers coverage with a fixed rate for the lifetime of the policy. The premiums are initially higher than anything associated with term insurance, but over your lifetime it is significantly less expensive to insure long term needs (think estate planning) with whole life coverage. There is also a cash value in whole life insurance that acts as a savings component that can be helpful throughout your life.

Universal Life Insurance: Universal life insurance is a unique product in one particular way. It will typically be set up so that you have a level insurance rate for the lifetime of the policy. There will also be a minimum and maximum amount of money you can deposit into the policy. The policy owner chooses an investment inside the policy and once a month the insurer dips into the investment account to withdraw the premium amount. If the investment grows there is the potential in the future to deposit smaller amounts of money, but the reverse is also true, if the value of the investment decreases you may need to make an extra premium deposit to keep things in force.

Life Insurance Rate Comparisons by Gender and Product Type

INSIGHTS

1. Short-Term Policies (10-20 years): For individuals seeking temporary coverage these policies offer the lowest monthly premiums.

2. Long-Term Policies (25-40 years): For individuals looking for extended coverage without switching policies. Premiums increase gradually for longer terms.

3. Lifetime Coverage: Whole life policies have higher premiums due to lifetime coverage.

Table: Life Insurance Rates by Product Type for Males

Details

Gender: Male

Actual Age: 30 Nearest Age: 30

Amount of Insurance: $100,000

Health Class: Regular, Non-Smoker

Quote Date: September 11, 2024

| Product Type | Lowest Rate Company | Monthly Premium | Yearly Premium |

| 10 Year Term | Manulife | $9.70 | $108.28 |

| 15 Year Term | Canada Life | $11.61 | $129.00 |

| 20 Year Term | Manulife | $11.34 | $126.61 |

| 25 Year Term | Beneva | $12.69 | $141.00 |

| 30 Year Term | Beneva | $13.77 | $153.00 |

| 35 Year Term | Canada Life | $18.00 | $200.00 |

| 40 Year Term | Canada Life | $21.31 | $236.80 |

| Term to age 65 | Industrial Alliance | $18.36 | $204.00 |

| Term of age 70 | RBC Insurance | $21.31 | $236.80 |

| Term to 100 Guaranteed Life Pay | Beneva | $61.47 | $683.00 |

| Whole Life Pay | Foresters | $60.03 | $667.00 |

| Whole Life Guaranteed Pay to 65 | Industrial Alliance | $80.19 | $891.00 |

| Whole Life Guaranteed 20 Pay | Foresters | $100.35 | $1,115.00 |

| Whole Life Guaranteed 15 Pay | Sun Life | $142.47 | $1,583.00 |

| Whole Life Guaranteed 10 Pay | Sun Life | $197.91 | $2,199.00 |

Table: Life Insurance Rates by Product Type for Females

Details

Gender: Female

Actual Age: 30 Nearest Age: 30

Amount of Insurance: $100,000

Health Class: Regular, Non-Smoker

Quote Date: September 11, 2024

| Product Type | Lowest Rate Company | Monthly Premium | Yearly premium |

| 10 Year Term | Manulife | $8.23 | $91.87 |

| 15 Year Term | Sun Life | $9.72 | $108.00 |

| 20 Year Term | Manulife | $9.69 | $108.13 |

| 25 Year Term | Beneva | $10.80 | $120.00 |

| 30 Year Term | Beneva | $12.15 | $135.00 |

| 35 Year Term | Beneva | $14.13 | $157.00 |

| 40 Year Term | Canada Life | $16.56 | $184.00 |

| Term to age 65 | Industrial Alliance | $14.22 | $158.00 |

| Term of age 70 | RBC Life Insurance | $16.56 | $184.00 |

| Term to 100 Guaranteed Life Pay | Industrial Alliance | $55.62 | $618.00 |

| Whole Life Pay | Foresters | $53.55 | $595.00 |

| Whole Life Guaranteed Pay to 65 | Industrial Alliance | $71.10 | $790.00 |

| Whole Life Guaranteed 20 Pay | Foresters | $88.74 | $986.00 |

| Whole Life Guaranteed 15 Pay | Sun Life | $129.69 | $1,441.00 |

| Whole Life Guaranteed 10 Pay | Sun Life | $173.52 | $1,928.00 |

Average Life Insurance Coverage in Canada – 2024 (CLHIA)

- The average life insurance coverage per household has increased from $474,000 in 2022 to $483,000 in 2024.

- Individual life insurance now makes up 65% of total policies in-force, driven primarily by term life insurance.

FAQs About Life Insurance Rates

Life insurance rates are determined using a number of factors combining actuarial data and personal information about the applicants health and lifestyle.

Your best bet is to contact an independent insurance broker who can take your information and shop it with various insurance carriers to find you the best life insurance rate.

The answer to this is very rarely. There have been situations where an insurer has originally interpreted health information and asked for a higher premium than the original quote (also known as a rated policy) where the independent advisor and the applicant have been able to explain the situation and have that extra premium amount removed, but this is rare. More often than not you are going to pay the rate that the insurer asks for.

At the beginning of the policy the life insurance rates for whole life coverage will be more money than the rates for term insurance. As time passes this will reverse as the term goes through a few renewal points.

Term life insurance policies will have a rate that increases over time. This happens when they hit their renewal points, and it will be laid out in the original policy when these points are and how much the life insurance rates will increase to.

You can improve your rates by improving your lifestyle and health. Making choices that improve your health will make it so that you can get better life insurance rates. An example would be choosing to quit smoking.

Your best route to doing this is to work with an independent insurance advisor like the team at lifeinsurancecanada.com. They will shop the marketplace with a variety of carriers for you and allow you to go to one point of contact to compare the rates from numerous companies all at once.

Conclusion

The way that life insurance rates are calculated isn’t all based in mystery. Remember, life insurance is a risk management tool where you transfer the financial repercussions of your dying unexpectedly on to the insurer. It only makes sense when you look at it like this that the insurer wants to know what type of a risk you pose to them. This makes it so they can calculate what the rates they will charge to take on this risk will be. Some of the risk factors you can’t control and some you can. Make sure that you understand how an insurer is going to calculate the premiums you will pay and how you can tilt the scales to your advantage. Working with the advisors at LifeInsuranceCanada.com can provide you with the guidance that you need to make sure that you get the maximum benefit from the premium dollars you commit to your life insurance policy.

Get a free quote

Over 200 Five-Star Google Reviews!